The NEW Daily Decision for 9.24.18 - Will Valuations Spoil The Bull's Party?

The State of the Markets:

In spite of the escalating trade "skirmish" and a long list of purported negatives, stocks continued to trudge higher last week with the DJIA finishing at a new all-time high on Friday. The S&P 500 wasn't far off the pace, closing just 0.04% off Thursday's record high. However, for the rest of the major indices, that's where the good news ended.

The bottom line is there are short-term divergences developing in the major indices as those seeing Ms. Market's glass as half-empty point out that the "troops" may not be following the "generals" at the present time.

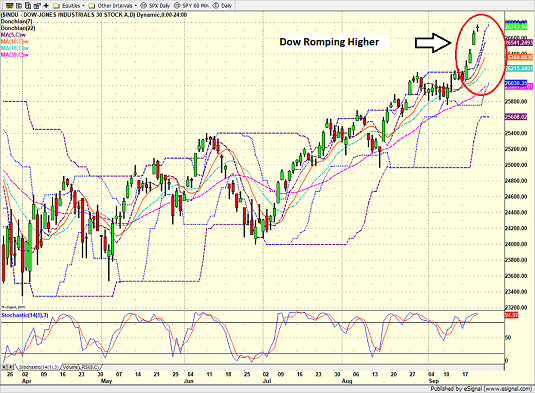

Let's start by looking at the good stuff on the chart of the Dow Jones Industrial Average (aka the original "generals" of the market)... Can you say "good times?"

DJIA - Daily

View Larger Image Online

As the saying goes, the most bullish thing a market can do is make new highs. 'Nuff said.

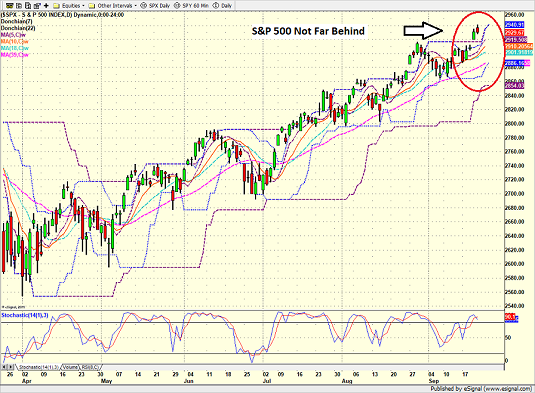

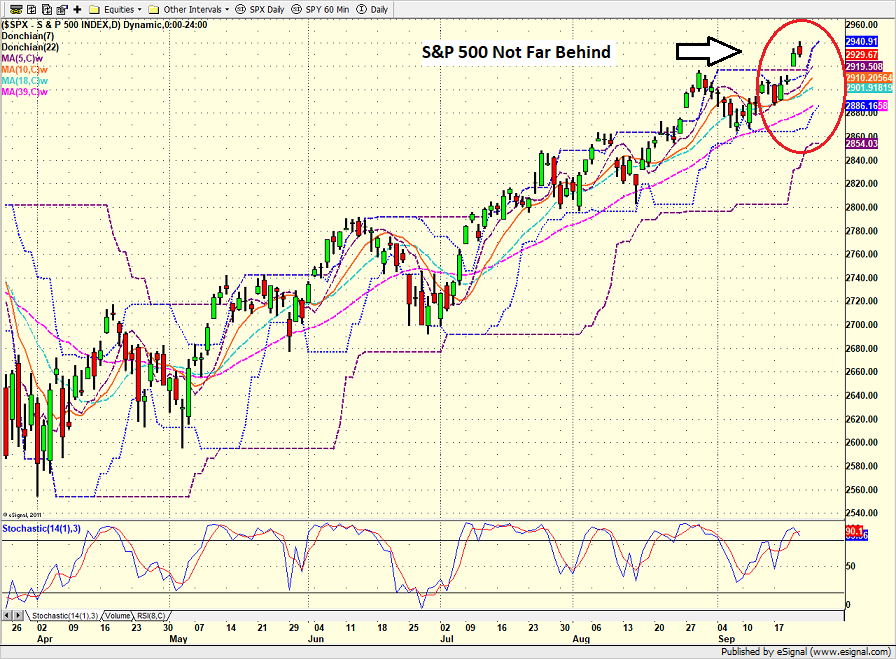

Next up is the S&P 500. While the Dow is romping to new highs, the action in the primary blue-chip index is not quite as encouraging. My take is good, but not great.

S&P 500 - Daily

View Larger Image Online

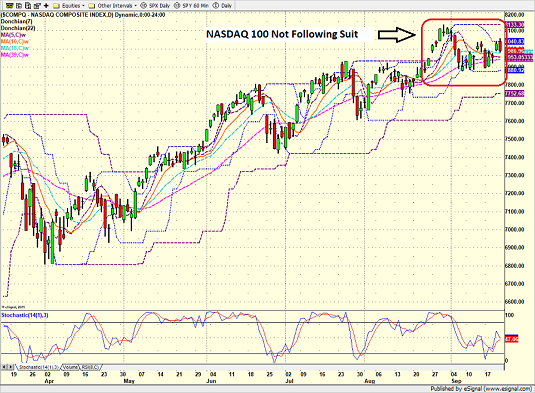

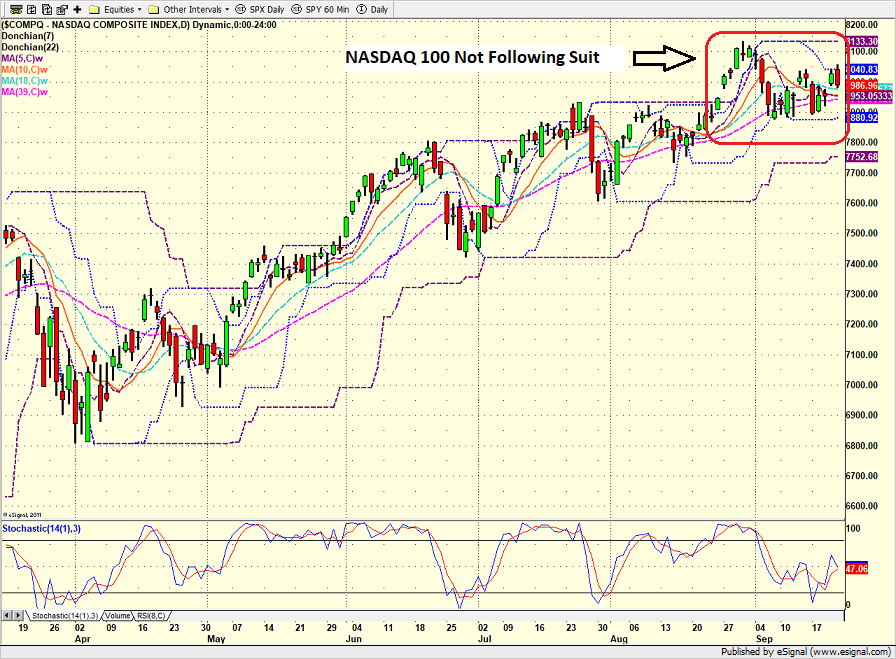

Now let's move on to the "troops". As the chart of the NASDAQ indicates, the market's long-term leaders do not appear to be following the Dow and S&'s lead. This week's sector rebalancing as well as some possible rotation away from the FANG's looks to be taking it's toll.

NASDAQ 100 - Daily

View Larger Image Online

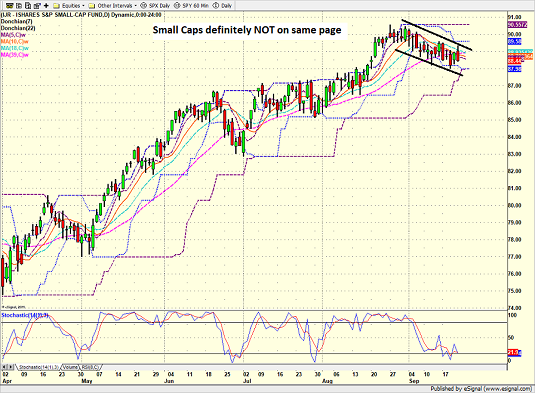

Then there are the small-caps. When you compare the charts of the DJIA and the IJR since the beginning of September, you have what amounts to a textbook example of a technical divergence.

iShares S&P Small-Cap (IJR) - Daily

View Larger Image Online

So, the first point I'd like to make on this fine Monday morning is that technical divergences CAN become problematic for the overall market over time. Not always. But, should the current divergent trends continue, our furry friends in the bear camp suggest that things may not end well for the bulls.

However, it is also important to note that short-term divergences are fairly common and may not last long. As such, it is probably not a good idea to run and hide at the present time due to the fact that small-caps are trending down slightly while the Dow is making new highs.

Can The Bulls Keep It Going?

The bulls point to the weekly charts of the Dow and S&P and ask simply, what's not to like? As such, the question of the day seems to be, how much higher can the current bull market run?

Obviously, nobody knows the answer to this question. Nor will I offer up an opinion on the subject. But I can say from experience that aging bulls tend to cause the bears a fair amount of pain as they often persist much longer than our furry friends can imagine.

While I'm not in the prediction business (sorry), I do believe that looking at some macro indicators can help determine whether or not the bears might wake up from hibernation sometime soon.

As I opined in last week's missive, entitled The Good, The Bad, and The Ugly, the economy, earnings, the labor market, and the state of the consumer lead the list of fundamental positives.

But if you asked 10 analysts to offer up their biggest negatives, I'd be willing to bet dollars to donuts that stock market valuations would be on every list. And since there has been a LOT of discussion on this recently, I'm going to spend the rest of my pixels this morning on the subject.

The Issue of Valuations

First up, I saw several references to the Price-to-Sales Ratio last week - which I highlighted as well in last week's report. The key point here is that the P/S Ratio recently exceeded the levels seen in 2000. Yikes.

Frankly, the folks yammering on about this stat are a bit late as my data shows the P/S, as well as most other traditional metrics, currently backing away from their recent highs. But, when looking at the Price-to-Earnings, Price-to-Dividend, and Price-to-Book Value indicators from a long-term perspective, there can be no arguing that all are at historically high levels.

Yet at the same time, it is also important to note that these metrics have been improving for much of the year. For example, as you are no doubt aware, the "E" in the P/E ratio has been "movin' on up" in 2018. And since price hadn't really done much until late summer, the P/E ratios have actually been trending lower.

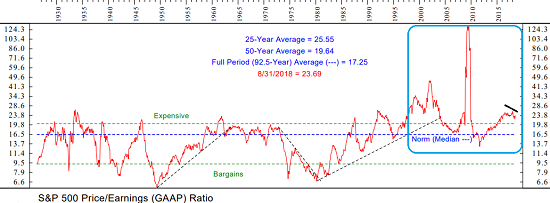

As Exhibit A here, I offer a long-term chart of the S&P's GAAP P/E Ratio - which is the P/E ratio using generally accepted accounting principles instead of the traditional earnings Corporate America reports on a quarterly basis (which tend to involve a fair amount of "financial engineering" and a bunch of non-recurring stuff that seems to show up with remarkable regularity).

S&P 500 GAAP P/E Ratio

View Chart Online

As you can see, the recent trend of the GAAP P/E is down. In short, this is good news if you are a stock market bull.

But the real question is whether the current readings are at extreme levels, which tend to give the bulls the edge, or something a bit less scary?

A Matter Of Perspective

From my seat, this is really a matter of perspective. As in, what time-frame are you looking at?

In the chart above, it is clear that the GAAP P/E remains well above the "Expensive" line (as determined by Ned Davis Research). However, this chart goes back into the 1920's. And as many bulls like to say, should we really be comparing today's market with anything that occurred before computers ruled the roost?

So, if you are bull or the manager of a mutual fund that, by prospectus, is required to stay nearly fully invested at all times, you may decide to change your "perspective" a bit. To something like the last 20 years. After all, 20 years is a pretty long time, right?

To help with this exercise, I've outlined the last 20 years in each of the charts in blue.

Now look at the GAAP P/E chart again. But this time, look only at the readings within the blue box. Voila. Suddenly valuations are not extreme. Heck, they aren't bad at all.

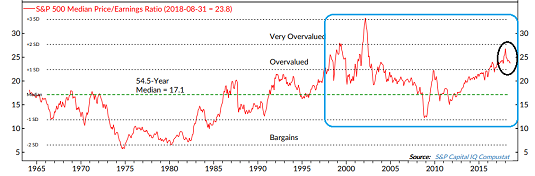

Next up, let's look at the Median P/E ratio, which looks at the P/E of the median stock in the S&P 500. I like this approach because it zeros in on the median stock within the S&P 500 instead of using the average of all stocks.

S&P 500 Median P/E Ratio

View Chart Online

Looking only at the data contained in the blue box, the median P/E appears to be a bit above the average over the last 20 years. While not cheap by any stretch, the point is the ratio isn't in nose bleed territory either.

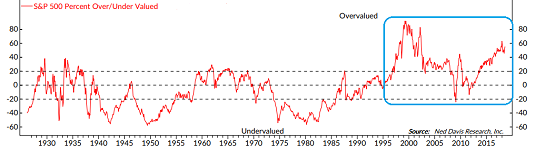

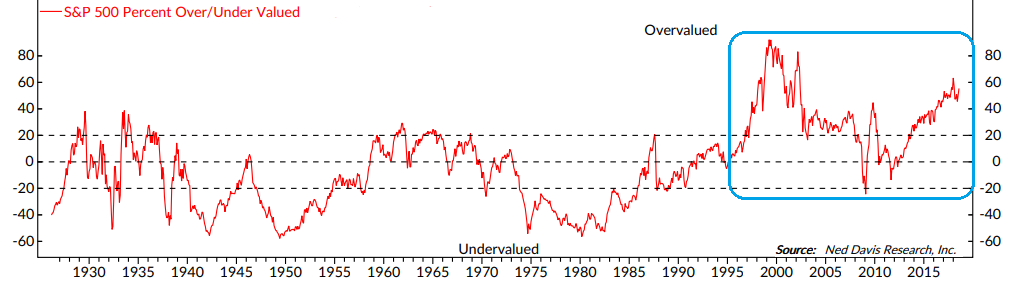

Finally, let's look at NDR's "Normalized Valuations" Model, which looks at long-term averages of six independent valuation indicators based on dividends, earnings, cash flow, sales, inflation-adjusted P/E and trend.

Normalized Valuation Model

View Chart Online

Looking at the entire series back into the 1920's, it is clear that stocks are currently at one of the most overvalued levels in history. And THIS is what the bears are fussing about.

But looking only the last 20 years, the picture is quite a bit different. While the model suggests that stocks definitely aren't cheap, they are also not at the extreme levels that the nattering nabobs of negativism have been screaming about.

The Bottom Line

There can be no arguing that the traditional valuation metrics are elevated relative to historical levels. But, depending on the time frame being used, one can argue that the market is not currently "extremely" overvalued.

Frankly, this approach to the valuation subject reminds me of an old saying... "There are three kinds of lies. Lies. Damned lies. And statistics."

But at the same time, there is an awful lot of money in the markets that is not "risk managed." Think about the trillions allocated to passive investing and the money that is simply automatically invested each month inside of 401K programs. This money is going to continue to be invested in stocks (well, up until it isn't, of course). But until then, I believe the passive craze suggests that another old saw may apply here: Valuations don't matter until they do - and then they matter a lot. And for now anyway, they don't seem to matter too terribly much. Party on, Wayne!

Have a great week!

Moving On... Now let's turn to the weekly review of my favorite indicators and market models... "But first a word from our sponsor ;-)"...

<hr>INTRODUCING: THE ELEVATION STRATEGY

A Tax-Efficient Risk Management Strategy for the U.S. Stock Market

Believed to be unique in the industry, the Elevation strategy is a long-term, risk-managed portfolio solution designed for growth-oriented investors seeking a tax-efficient, risk-managed approach to the stock market. Our tests show that 75% of the Strategy's profitable trades since 3/31/1999 would have qualified as long-term for tax purposes.

<hr>The State of the Big-Picture Market Models

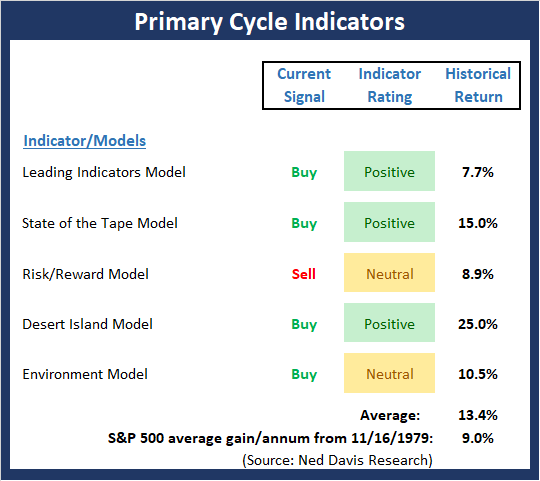

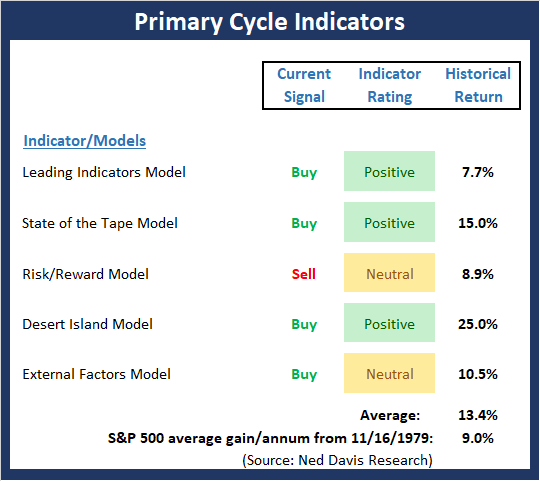

I like to start each week with a review of the state of my favorite big-picture market models, which are designed to help me determine which team is in control of the primary cycle.

View My Favorite Market Models Online

The Bottom Line:

- The Primary Cycle board upticked a bit this week as the Leading Indicators Model moved up a smidge from high-neutral to moderately positive. In order to gauge the overall "tone" of the board, we have decided to begin reporting the mean and median reading of the models each week. This week's mean percentage score of my 5 favorite models is 62% while the median is 65%. We will expand on this analysis in the coming weeks

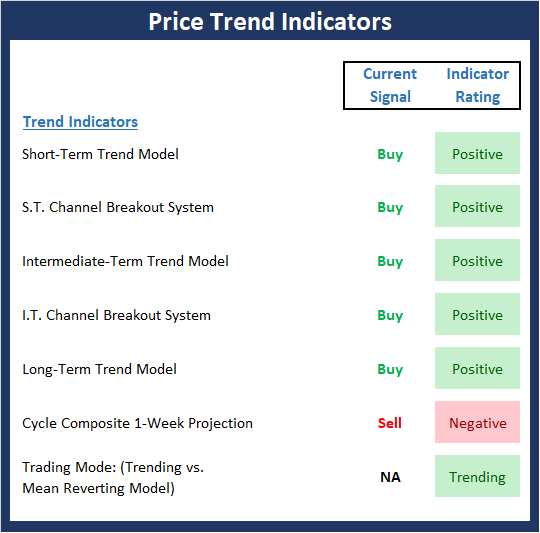

The State of the Trend

Once I've reviewed the big picture, I then turn to the "state of the trend." These indicators are designed to give us a feel for the overall health of the current short- and intermediate-term trend models.

View Trend Indicator Board Online

The Bottom Line:

- With the Dow and S&P finishing the week at all-time highs, it makes sense that the Trend Board is in good shape. The "yea, but" here is the recent action seen in the NASDAQ, mid-caps, and small-caps - which are actually in a downtrend at this time. As such, I can argue the troops are not following the generals from a near-term perspective, which is something to watch going forward.

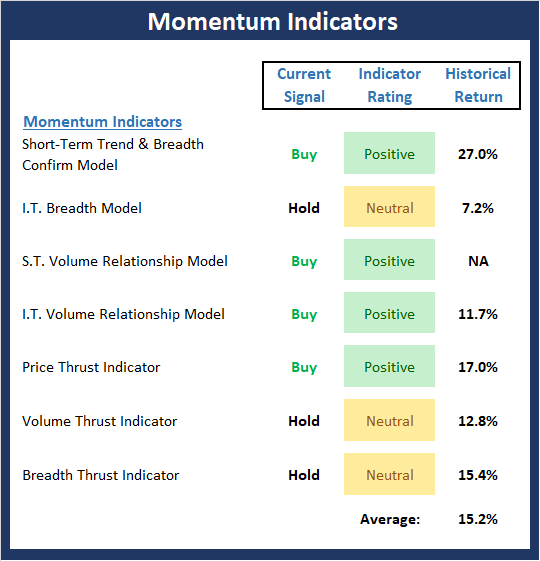

The State of Internal Momentum

Next up are the momentum indicators, which are designed to tell us whether there is any "oomph" behind the current trend.

View Momentum Indicator Board Online

The Bottom Line:

- Despite the new highs seen in the blue-chip indices, the Momentum board downticked slightly last week as our Intermediate-Term Breadth model slipped into the neutral zone. This represents a slight divergence and remains something to watch as the market exits the seasonally week period in a few weeks.

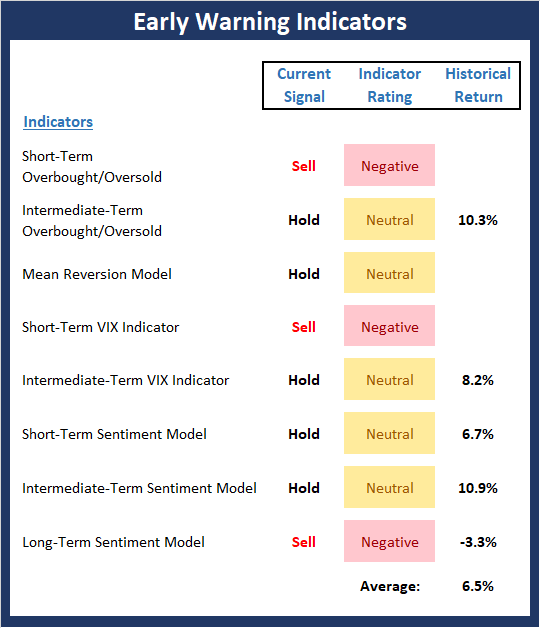

The State of the "Trade"

We also focus each week on the "early warning" board, which is designed to indicate when traders might start to "go the other way" -- for a trade.

View Early Warning Indicator Board Online

The Bottom Line:

- The message from the "Early Warning" board would seem to be one of caution. While there are not enough outright sell signals to give the bears a clear edge, the overbought condition coupled with the divergences seen in trend and momentum provides, at the very least, a reason to raise an eyebrow.

The State of the Macro Picture

Now let's move on to the market's "environmental factors" - the indicators designed to tell us the state of the big-picture market drivers including monetary conditions, the economy, inflation, and valuations.

View Environment Indicator Board Online

The Bottom Line:

- The External Factors board continues to be a hot mess. The recent spike in rates has caused the Monetary Composite (a combination of two monetary models) so slip into the negative zone. The bottom line here seems to be that while earnings may be the "lifeblood" of the stock market, the external factors present the bulls with, at the very least, a significant headwind.

Thought For The Day:

The greatest deception men suffer is from their own opinions -- Leonardo da Vinci

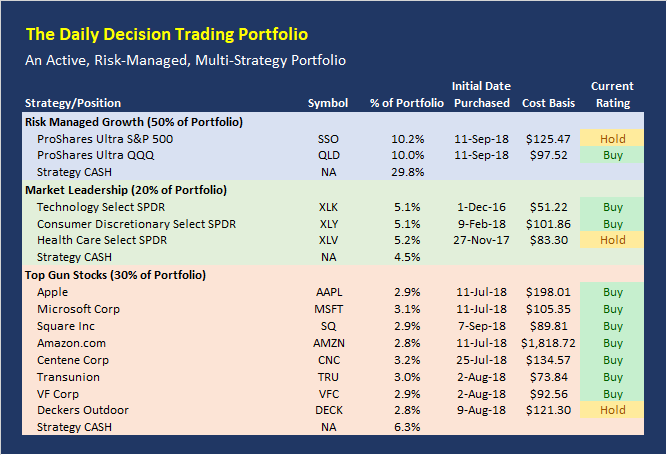

The NEW Daily Decision Portfolio

The latest upgrade to the Daily Decision service went live on Monday, July 9. The new, state-of-the-art portfolio is a hedge fund approach incorporating multiple methodologies, multiple strategies, and multiple time-frames, which is comprised of three parts. The structure of the portfolio is as follows:

- 50% Aggressive Risk-Managed Growth (up to 200% long)

- 20% Market Leaders

- 30% Top Gun Stocks

The Aggressive Risk-Managed Growth portion is made up of three trading strategies and accounts for 50% of the portfolio. The Market Leadership portion makes up 20% of the portfolio. And the Top Guns Stocks portion (10 of our favorite stocks) will make up the final 30% of the portfolio.

All three of our strategies are run in a single Marketfy model - the model is currently labeled as the LEADERS model. The goal is to make the service simpler to follow by putting everything in one place.

Today's Portfolio Review:

Current Rating Explained

This is our rating for the day. The Current Rating tells you what action we would take if we did not currently hold the position. A "Buy" rating means we would be willing to purchase the position at current prices. A "Strong Buy" suggests this would be our first choice to buy. A "Hold" rating indicates we would not make new purchases at current levels. And a "Sell" rating indicates we will likely exit the position in the near-term.

Positions Can Change

Positions often change during the trading session. Remember that we will send a Trade Alert via SMS Text Message and/or Email BEFORE we ever make a move in the models.

Disclosure

At the time of publication, the editors hold long positions in the following securities mentioned:

SPY, IJR, QQQ, XLK, XLY, XLV, AAPL, MSFT, AMZN, CNC, TRU, VFC, DECK, SQ

- Note that positions may change at any time.

Wishing You All The Best in Your Investing Endeavors!

The Front Range Trading Team

NOT INVESTMENT ADVICE. The analysis and information in this report and on our website is for informational purposes only. No part of the material presented in this report or on our websites is intended as an investment recommendation or investment advice. Neither the information nor any opinion expressed nor any Portfolio constitutes a solicitation to purchase or sell securities or any investment program. The opinions and forecasts expressed are those of the editors and may not actually come to pass. The opinions and viewpoints regarding the future of the markets should not be construed as recommendations of any specific security nor specific investment advice. Investors should always consult an investment professional before making any investment.

Recent free content from FrontRange Trading Co.

-

The Lines In The Sand Are Clear

— 9/16/20

The Lines In The Sand Are Clear

— 9/16/20

-

The Question of the Day

— 8/04/20

-

Portfolio Update: 1.23.20

— 1/23/20

-

State of the Markets: Modeling 2020 Expectations (Just For Fun)

— 1/13/20

-

Current Holdings for ALL-NEW 2020 Daily Decision Model Portfolio

— 1/03/20

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}