The Waiting Game

Modern times demand modern thinking in portfolio design. Learn more...

Since I received a fair amount of positive feedback on my "executive summary" of the market broken out by time frame, I thought I'd provide another update this morning. It is my sincere hope that you might find a nugget or two in the following assessment of market conditions/drivers.

SHORT-TERM (1-30 Days)

Unless you have been living in a cave without access to internet or even a cell phone, you are likely aware that on the day after tomorrow, the U.K. will vote on whether or not to stay in the European Union. Prognostications are all over the map on this one with folks like George Soros calling for the end of the world should the "Leave" vote carry the day while others suggest that "Bremain" is already priced in.

Digging into the meat of the issue, I think the big fear is that if the vote favors a "Brexit," asset flows will follow suit. In other words, traders worry that if Britain votes to leave the EU, money will flow out of the country's banking system en masse. As such, this explains why the banks have been in focus across the pond for some time now. And on that note, remember that all is not well with the banks of Europe and that large amounts of money flowing in the wrong direction could produce, as the British might say, a prickly situation. So, investors should watch the action in the banks as a "tell" for what to expect next.

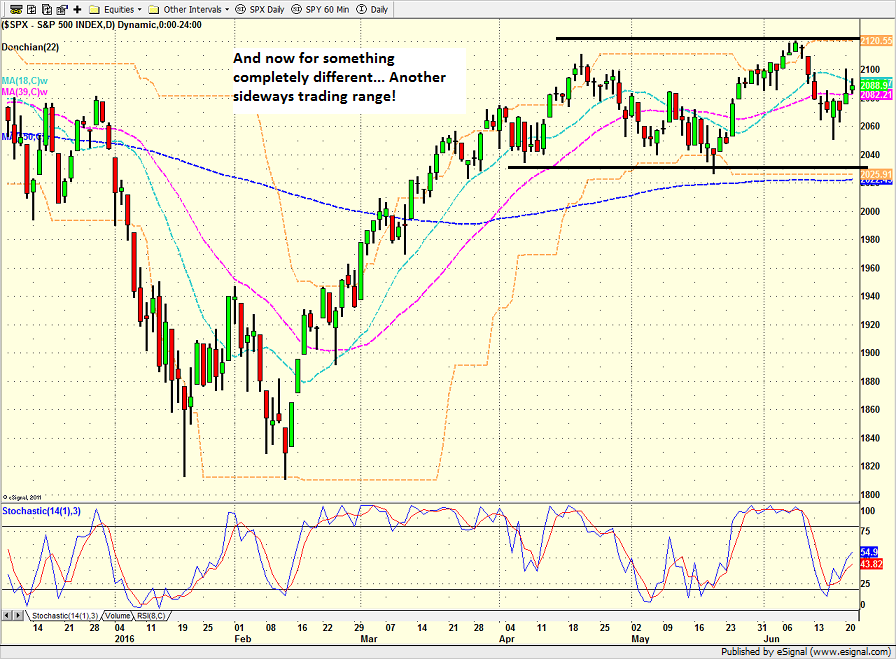

Before leaving the subject, it is also worth noting that the stock market is really none the worse for wear in the face of the Brexit uncertainty. With just one day before the vote, the major indices are just a stone's throw from all-time highs. And while I don't claim to be a pure market technician, the current sideways action on the chart of the S&P 500 does suggest that stocks are playing a waiting game.

S&P 500 - Daily

View Larger Image

Here at home, Janet Yellen and her merry band of central bankers remain the focal point. While I'm not sure how many more ways Ms. Yellen can say that the FOMC is not likely to raise rates in the near-term, markets do tend to react each and every time the Fed Chair gets near a microphone. Based on my read, the futures market currently projects only a 5% chance of a rate hike at the July FOMC meeting and just a 24% probability that rates will rise at the September meeting. Thus, the uncertainty of when the Yellen & Company will take action is also contributing to the sideways action in the near-term.

INTERMEDIATE-TERM (2-6 months)

After the June 23 Brexit vote, the next "big, bad event" on the calendar is the U.S. Presidential election in November. Contrary to popular belief, the market doesn't really care which party wins the election. Sure, history shows that the market tends to do better when the incumbent party wins. However, this election in particular is shaping up to be historic on many fronts. And with the presumptive Republican candidate being a bit of a wild card, stocks could easily remain trapped in uncertainty mode (remember, the stock market hates uncertainty!) until it becomes clear which party is going to win the White House. The good news is that this particular uncertainty has a defined time line.

Speaking of time lines, it is also a positive from an intermediate-term perspective that our cycle work suggests that a summer rally is likely to continue until the middle of August. After that, one could argue that either election or economic uncertainty could create the traditional September swoon. But given all the various uncertainties in play at the present time, it is likely a good idea to stay on your toes and be ready to buy the dips.

LONG-TERM (>6 months)

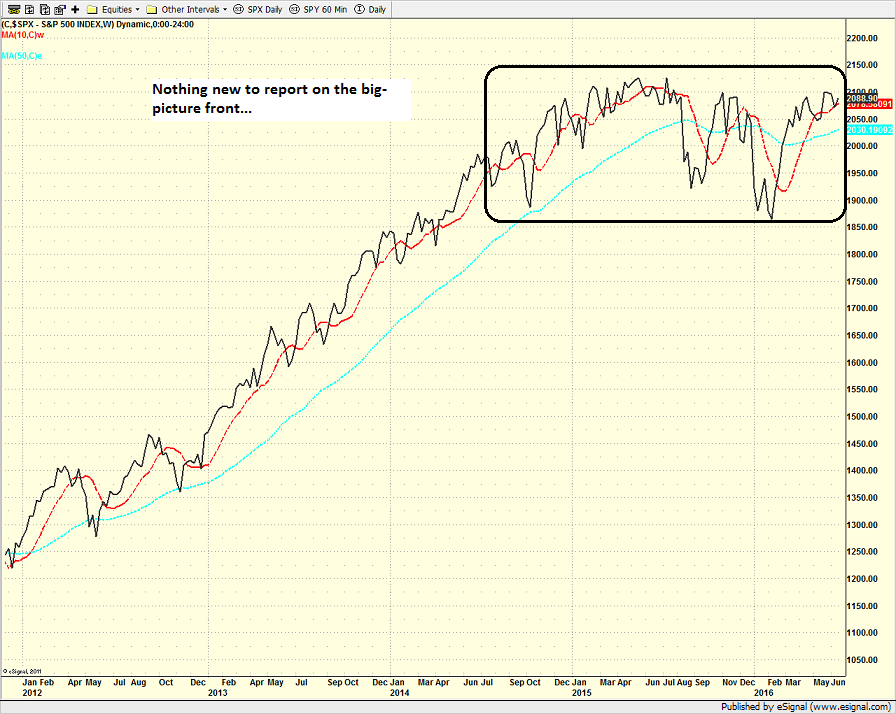

From a longer-term perspective, there is nothing much new to report. From my seat, the stock market remains stuck in what I see as a sideways, consolidation pattern due to all the macro uncertainties. Issues such as growth in the U.S. and global economies, the state of corporate earnings, and the level of stock market valuations have caused both teams to curb their enthusiasm whenever the market approaches important levels. As I've said before, stock market declines are cut short due to global central bank intervention while rallies are being kept in check due to valuations.

S&P 500 - Weekly

View Larger Image

The bottom line appears to be that absent the type of multiple expansion seen in the late 1990s/early 2000, stocks may not have a lot of upside potential based on the current valuation levels. While the valuation game is (a) very tricky and (b) a lousy timing indicator, it is worth noting that median P/E levels continue to rise and save the bubble era, have never been substantially higher than they are now.

Therefore, we can argue that stocks will be reliant on earnings growth for any upside beyond the current high water mark. But given that we also believe stocks are in the midst of a secular bull market, this continues to be a "buy the dips" market environment.

Current Market Drivers

We strive to identify the driving forces behind the market action on a daily basis. The thinking is that if we can both identify and understand why stocks are doing what they are doing on a short-term basis; we are not likely to be surprised/blind-sided by a big move. Listed below are what we believe to be the driving forces of the current market (Listed in order of importance).

1. The State of the "Brexit"

2. The State of U.S. Economic Growth

3. The State of Fed Policy

4. The State of the Stock Market Valuations

Thought For The Day:

"Breathe. Believe. Battle." Keri Walsh Jennings

Here's wishing you green screens and all the best for a great day,

David D. Moenning

Founder: Heritage Capital Research

Chief Investment Officer: Sowell Management Services

Looking for More on the State of the Markets?

!function(d,s,id){var js,fjs=d.getElementsByTagName(s)[0],p=/^http:/.test(d.location)?'http':'https';if(!d.getElementById(id)){js=d.createElement(s);js.id=id;js.src=p+'://platform.twitter.com/widgets.js';fjs.parentNode.insertBefore(js,fjs);}}(document, 'script', 'twitter-wjs');Disclosures

The opinions and forecasts expressed herein are those of Mr. David Moenning and may not actually come to pass. Mr. Moenning's opinions and viewpoints regarding the future of the markets should not be construed as recommendations. The analysis and information in this report is for informational purposes only. No part of the material presented in this report is intended as an investment recommendation or investment advice. Neither the information nor any opinion expressed constitutes a solicitation to purchase or sell securities or any investment program.

Any investment decisions must in all cases be made by the reader or by his or her investment adviser. Do NOT ever purchase any security without doing sufficient research. There is no guarantee that the investment objectives outlined will actually come to pass. All opinions expressed herein are subject to change without notice. Neither the editor, employees, nor any of their affiliates shall have any liability for any loss sustained by anyone who has relied on the information provided.

The analysis provided is based on both technical and fundamental research and is provided "as is" without warranty of any kind, either expressed or implied. Although the information contained is derived from sources which are believed to be reliable, they cannot be guaranteed.

David D. Moenning is an investment adviser representative of Sowell Management Services, a registered investment advisor. For a complete description of investment risks, fees and services, review the firm brochure (ADV Part 2) which is available by contacting Sowell. Sowell is not registered as a broker-dealer.

Employees and affiliates of Sowell may at times have positions in the securities referred to and may make purchases or sales of these securities while publications are in circulation. Positions may change at any time.

Investments in equities carry an inherent element of risk including the potential for significant loss of principal. Past performance is not an indication of future results.

Advisory services are offered through Sowell Management Services.

Recent free content from FrontRange Trading Co.

-

Is The Bull Argument Too Easy These Days?

— 8/31/20

Is The Bull Argument Too Easy These Days?

— 8/31/20

-

What Do The Cycles Say About 2020?

— 1/21/20

-

Modeling 2020 Expectations (Just For Fun)

— 1/13/20

-

Tips From Real-World Wendy Rhoades

— 5/06/19

-

The Best Recession Ever!

— 4/29/19

-

{[comment.author.username]} {[comment.author.username]} — Marketfy Staff — Maven — Member

{kind=link}

{kind=link}

- 1 Campus Martius, Suite #200Detroit, MI 48226

- +1 877 440 9464