THE WEEKLY TOP 10

If you would like to get comments like these each weekend...and get a daily note on the short-term term aspects of the broad market, different sectors and specific stocks, please click here to subscribe to The Maley Report.

THE WEEKLY TOP 10

Table of Contents:

1) The Fed’s change in stance is much more important than the omicron variant.

2) The Fed is telling us that they have has moved the “safety net” to a lower level.

3) BOTH the U.S. & China have shifted their policies dramatically this year.

4) The set-up in the marketplace as we moved into Thanksgiving week was not a good one.

5) “Gamma” and “momentum based algos” work in both directions.

6) The cracks in “other” markets are growing.

7) The euro/yen cross is sending out a warning signal as well.

8) Support/resistance levels for the S&P 500, Nasdaq and Russell 2000.

9) Where’s MY offer to coach a Division I college football team?

10) Summery of our current stance….Don’t fight the Fed (or China).

1) We’re going to take a different tact this weekend. A couple of weeks ago, we stated that the stock market was a very unhealthy one…so much so that we took the position that we were headed for a bear market in 2022. The developments of the past few weeks have only emboldened our stance. This weekend, we’ll review why we believe the “set-up” in recent months (and even years) has made a bear market likely next year…and then we’ll talk about how the more recent developments have now made it a highly likely outcome.

For those who read out work regularly, some of this will be a bit repetitive, but we wanted to put our entire thought process on display this weekend…as we move into the end of the year and into 2020.

First of all, one of our main themes says the massive monetary and fiscal stimulus of the past 21 months has pushed the stock market WELL ABOVE its underlying fundamentals. Therefore, we don’t have to see a significant slowdown in economic or earnings growth in order to expect a significant decline in the stock market.

Yes, this makes today’s situation quite unique. Traditionally, economist and strategists have studied the economy and earnings growth for signals about the stock market’s future direction…for the simply reason that the stock market was traditionally driven buy what it saw in terms of growth about 6-9 months into the future. (The market was forward looking. When it saw growth in the future, it rallied…and vice versa.)……..HOWEVER, over the past dozen years…and ESPECIALLY over the past 21 months (since the March 2020 pandemic lows)…it has been the stock market itself that has been the driver for the economy, not the other way around!

The MASSIVE levels of monetary stimulus from the global central banks…and the massive levels of fiscal stimulus from many countries around the world…took the stock market WELL ABOVE the underlying fundamentals during the summer of 2020. Nobody disputes that the big rally in the stock market in the spring and summer of that year took the market up (and held it up) to a level that was much higher than the economy/earnings would have justified…because the economy has all but totally shut down!!!! Everybody believed it was the right thing to do. The huge level of stimulus was needed to push the markets to artificial levels…in order to offset the SHORT-TERM economic/financial emergency that we were facing.

The thinking was that this artificial stimulus would “build a bridge” to the other side of the “valley” of the pandemic. Most people believed that vaccines would be developed (or that heard immunity would be reached) before too long. Once the pandemic came under control, the economy would quickly play catch-up to the stock market…which was being held up by the stimulus. THEN, everything would be hunky dory.

The problem is that most bridges start and end at the same elevation. However, the pandemic bridge that was provided by monetary and fiscal stimulus took the market to a level that was MUCH HIGHER than where it started (when the pandemic began). In other words, the emergency levels of stimulus that had existed during the emergency phase of the pandemic…remained in place long after the emergency had passed. THEREFORE, even though the economy DID play catch-up to a certain degree (especially in late 2020 and early 2021), it could not play catch up to a degree that put it anything close to where the stock market is trading today. After the initial jump, the stock market kept on rallying at the same pace the economy and earnings were improving…so they were never able to fully catch up to the stock market (not even close).

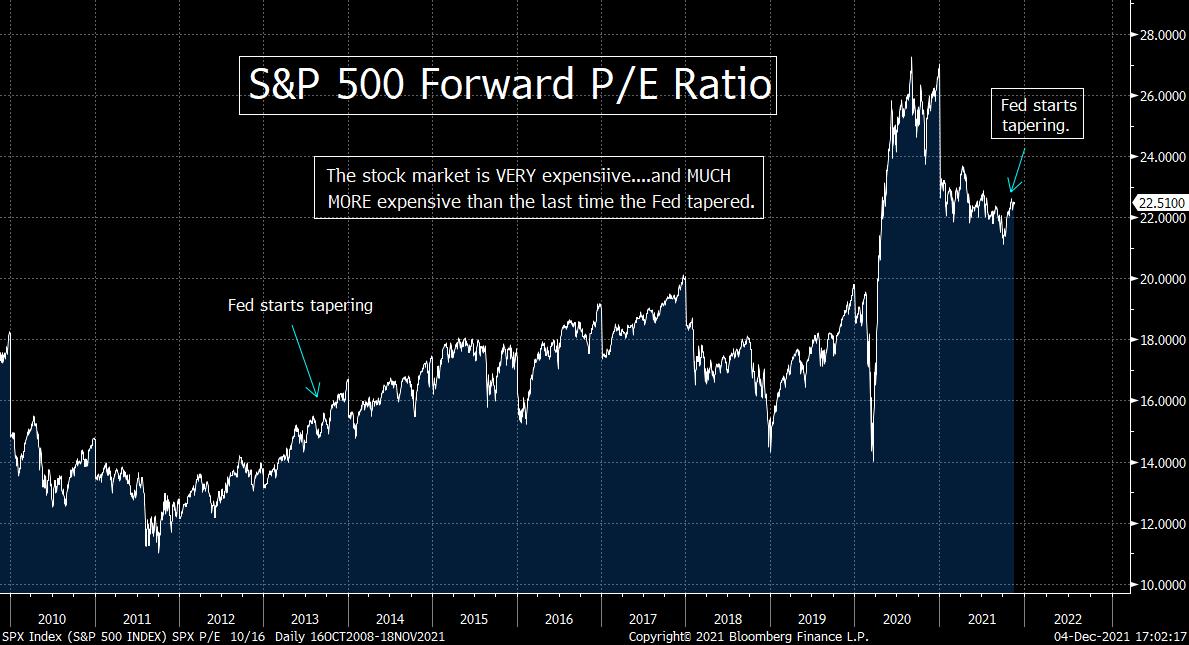

One only has to look at the valuation of the stock market to see how it was VERY far ahead of the underlying fundamentals. The S&P 500 was trading at 21.5x forward earnings at its November peak…and more than 3x sales (the most expensive reading on that indicator EVER)…….Sure, people argued that these high levels of valuation are fine…because long-term interest rates are so low. However, the last two times the yield on the long bond stood at 1.6% (in 2016 and 2019), the forward P/E for the S&P 500 was just 18x earnings…and about 2.2x earnings!!! To reach those levels, the S&P would have to fall below 4,000 (and that’s only if rates don’t rise any further).

(We would also highlight that the stock market has been a key diver for the economy for over a decade…not just the past few years. Back in the years immediately following the financial crisis, the (then) Fed Chairman Bernanke said publicly that the goal of the Fed was to push asset prices higher (especially stocks)…with the goal of it helping the economy. Therefore, it became a situation where the moves in the stock market were the catalysts for the moves in the economy…not the other way around.)

This correlation returned after the pandemic all but completely shut down in the first quarter of 2020…and (more importantly), the financial markets (fixed income markets) started to freeze up again. (Most people do not realize that the financial system was staring into the abyss in March of 2020 to the same degree it was in 2008. That is NOT an exaggeration!!!!!!!)

However, as we came out of the financial crisis, the financial system was in much worse shape. Therefore, the Fed kept having to provide liquidity for many, many years…to make sure Humpty Dumpty didn’t roll back over and fall again. The (still) fragile system a decade ago is the reason that the huge level of monetary stimulus did not create high levels of inflation (the way many pundits assumed it would).

This time, however, the system HAS recovered very quickly. Therefore, the massive levels of stimulus (much more than the supply chain issues)…HAVE created a high level of inflation this time around. Thus, the Fed cannot just keep on pumping like crazy….like they did for several years following the Great Financial Crisis.

Instead, they’re going to have to tighten policy. The bad news is that this will create significant headwinds for this extremely expensive stock market…and we believe it will create a bear market next year. (It might have already started.) However, the good news is that the financial system has a much better chance of withstanding a deep correction or even a bear market…than it did a decade ago. Therefore, the decline in asset prices will actually be normal and healthy…and will allow the markets to regain their footing more quickly than if the Fed kept pumping like crazy…and created a 1999/2000 style bubble (or bigger).

2) As you can gather from what we said in point #1, we believe that the new developments in the Covid-19 situation played a much smaller role in last week’s big pickup in volatility in the stock market…than the confirmation from the Fed that they are moving away from “gradualism” when it comes to their new tightening policy. This is key…because the omicron variant could fade quickly…while the Fed’s new tightening cycle won’t.

We believe that those who are focused on the omicron variant when they try to decipher what is going to happen in the markets in the coming weeks (and into 2022) are completely missing what’s really going on in the economic/financial landscape today. The real “new development” of the last week has been the shift by the Fed away from “gradualism” in their tightening policy…to a much more aggressive stance.

It was interesting that the many on Wall Street are focusing on the development of the omicron variant of Covid-19 as the reason for the mild pullback in the market we have seen recently. We understand why the focus was on this issue…because the first big “one-day decline” took place the day after Thanksgiving…when the concerns surrounding this variant first became public. However, there’s another reason to why many are focused on this issue: The odds are much better that the omicron issue will go away a lot more quickly than the other key development from last week. Therefore, they can maintain their perma-bullish stance when they talk to investors.

In reality the much more important development from last week was the confirmation from the Federal Reserve that they are abandoning their strategy of extreme “gradualism” when it comes to their new tightening policy…to one where they are going to be much more aggressive. The narrative went from one that said there is no way that the Fed would speed up its tightening moves (in either taper or rate hikes) with the new-news on the omicron variant on Monday…to having it put back right in the middle of the table by Chairman Powell on Tuesday and Wednesday.

Not only did the Fed Chairman say that the omicron variant would not cause them to pause, but it could also actually lead them to speed up the process!!!! A lot of people thought he would pullback from those comments during his second day of testimony (like he has in the past…when his comments were initially construed as hawkish). Instead, he doubled down. He repeated that the risks of persistent, higher inflation have “moved up”….and that the Fed is not abandoning the view that current inflation spike will require a meaningfully different monetary policy response than currently envisioned over the next couple of years. (Repeat, “Next couple of years”!!!)…..Finally, he said, “We’ll use our tools to make sure this high inflation we’re experiencing won’t become entrenched.”…….In other words, he did A LOT more than just take the term “transitory” out the lexicon.

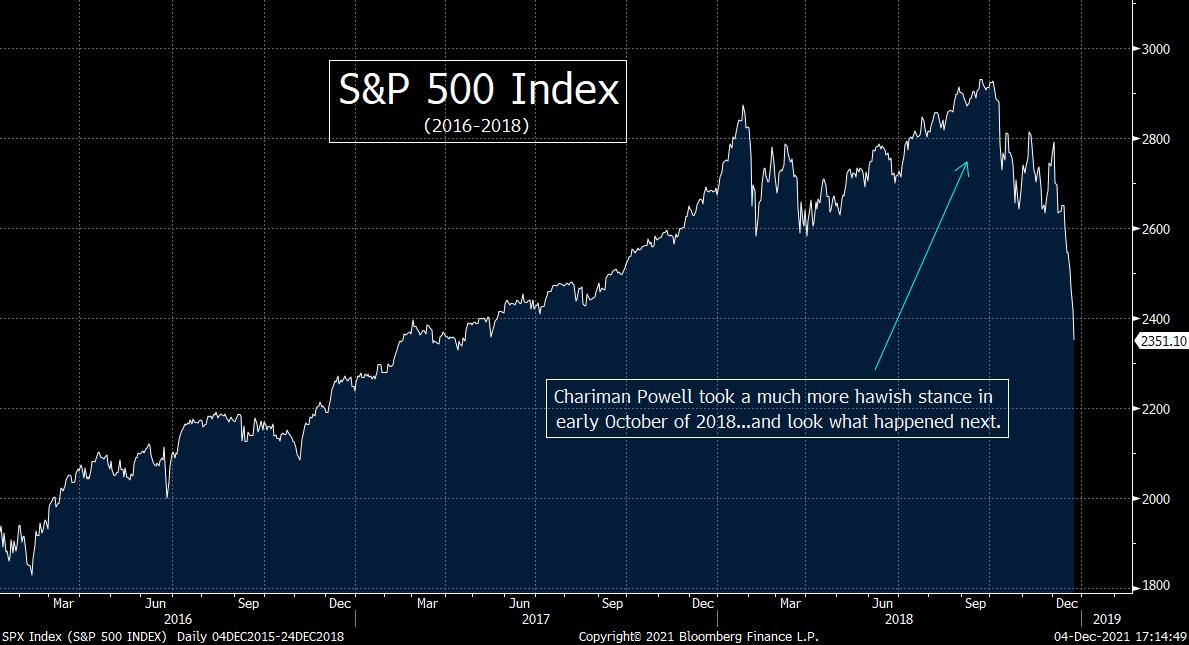

This is very reminiscent of the 4th quarter of 2018. As we moved into October of that year…and Mr. Powell started talking about their tightening cycle in a much more hawkish fashion. (I remember the comment clearly…when he said on October 3rd of that year, “We’re a long way from neutral.”) Almost immediately, the stock market began a deep correction that took the market down by over 19% over the next three months. As we stated at the time, the Fed KNEW that their tightening cycle would create problems for stocks and other risk assets, but they kept on tightening (and kept speaking in a hawkish manner). They stated publicly that year that they were worried about valuations (“bubble”)…which meant that they wanted to let some air out of the markets. It was not until the credit markets started to see some serious stress…that the Fed reversed course.

In other words, back in 2018, the Fed still had a nice “safety net”…and nice “Fed put.” HOWEVER, by tightening, the Fed moved that “put” to a level that was much more “out of the money” than it had been for many years following the credit crisis. Said another way, they had moved their “safety net” to a much lower level than it had been in the past. We believe the Fed has done the same thing this time.

The situation IS a bit different. In 2018, the Fed was trying to avoid a bubble. This time, they’re likely trying to avoid a bubble as well, but the more important issue is inflation. In other words, they HAVE to start tightening…..That said, the Fed KNOWS it will create problems for risk assets for a period of time. They’re okay with this (as they should be)…healthy markets do not go up in a straight line. Corrections…and even bear markets are normal and healthy in a capitalistic system.

The message to investors: Don’t fight the Fed.

3) We now have a situation where the central bank of the world’s biggest economy going from a very gradual move towards tightening…to (now) a situation where they are going to a more aggressive tightening timeline. ALL OF THIS IS TAKING PLACE at a time when the world’s second largest economy is going from STRONGLY encouraging high levels of debt, leverage and risk taking…to one where they are clamping down on all three!!!

There is no question in our minds that a dramatic shift has taken place for the countries with the two largest economies in the world. As we have highlighted above, in the world’s largest economy (the U.S.), the Fed has moved from an ultra-accommodative policy…to one of tightening.

We do admit that just because the Fed has become more aggressive with their tightening cycle, that does not mean that they are now engaged in a highly aggressive policy. However, tapering IS tightening…and short-term rates ARE going to be moving higher next year (unless another major crisis develops). When a central bank goes from a MASSIVE stimulus policy…to one of tightening…it’s STILL a significant change. This is especially true when the change takes place in an extremely expensive market.

(We say that “tapering IS tightening” because we believe that the artificial stimulus that is added to the system is like the artificial stimulus steroids give a weightlifter. If/when a weightlifter starts weening off his/her steroids, it does not take long for that person to become weaker. When they come off the steroids completely, they become MUCH weaker. That doesn’t mean they won’t be able to lift a lot of weight. Heck, they’ll still be lifting weights on a regular basis. However, they will definitely not be able to lift the same level of weights as they did when they were under the influence of steroids.)

The world’s second largest economy, China, has also change their policies in a significant way in the last year. That’s right, BOTH the U.S. and China have been making shifts over the last year. China began late last year when the cracked-down on Alibaba. They then continued to follow this crackdown in a pretty aggressive manner as we moved through 2021. They extended the crackdown from to many other tech stocks…and then moved to real estate, education, casino, video gaming companies, etc. (The U.S. began January of this year…with Atlanta Fed President Bostic laying the groundwork for their first taper move. However, the U.S. shifted in a much more gradual way…as other Fed officials changed their rhetoric to a more hawkish stance over many months. However, that all changed in the past couple off weeks…especially this past week. They have confirmed that they’re going to be much more aggressive than they had been saying over the summer.)

For China, they have gone from encouraging debt, leverage and risk taking in a major way for MANY years…to one where they are now clamping down on all three facets…in a significant way. So there is no question that the world’s second largest economy has made a substantial change in the way they do things in 2021.

For YEARS we have been hearing, “Don’t fight the Fed” and “Don’t fight China.” Those sayings have worked very, very, very well for investors since the financial crisis. However, these two economic powers have COMPLETELY shifted their strategies in 2021…and thus investors NEED to shift the way they look at the markets.

What we’re saying is that if somebody tells you that you don’t have to worry…because the omicron variant is not going to be a big problem, you should respond by saying, “So what!”……Don’t get us wrong, if the problems surrounding the omicron variant fade quickly, the stock market should see a short-term bounce…one that might even last a few weeks. However, the major changes that have taken place in the U.S. and China this year means that the intermediate & longer-term headwinds facing the stock market right now are not going to subside much at all if/when the pandemic issues eventually fade.

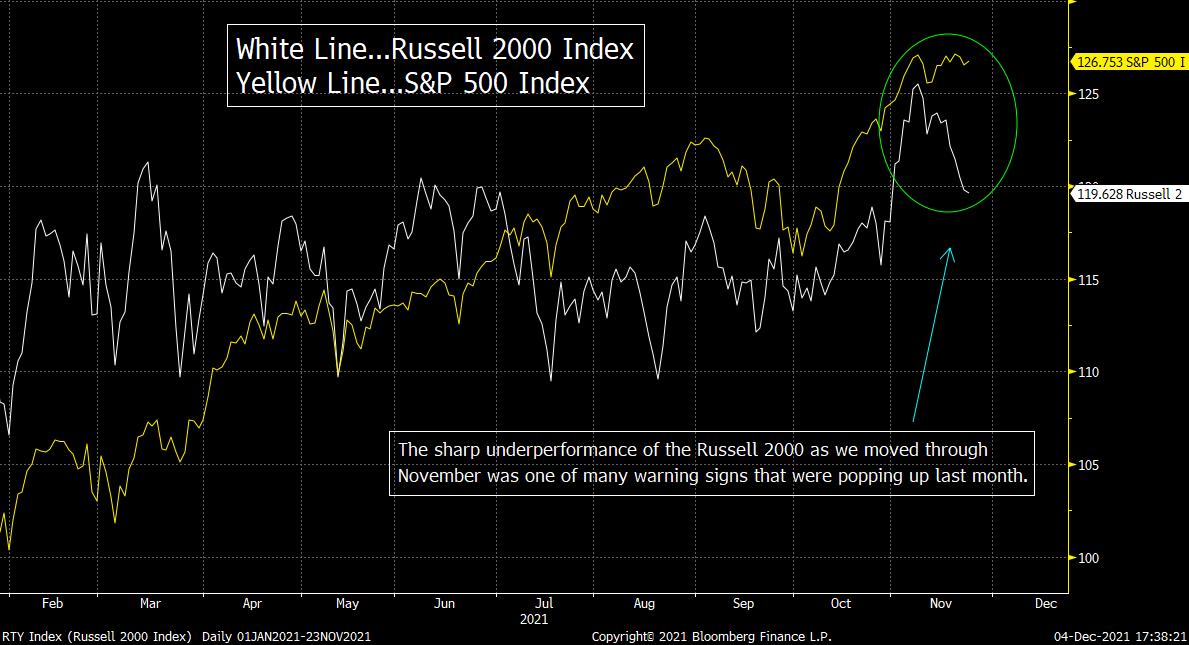

4) The set-up in the marketplace as we moved into Thanksgiving week was not a good one. The major indices had become quite overbought…the rally had become much more narrow…the froth in the marketplace was becoming extreme again…and earnings growth expectations had ground to a halt. Therefore, the stock market was already becoming ripe for a pullback even before the Fed confirmed their much more hawkish stance.

In some ways, the market should not have been shocked by Chairman Powell’s comments last week. Several other members of the FOMC had been saying for weeks that the Fed should speed p their tapering process…and some had even talked about a quicker timetable for raising short-term rates. However, the markets have learned not to get excited about the timing of any change in attitude/policy from the Fed until the Chairman confirms the change. Therefore, we’re not surprised at all that the markets did not react until this past week (when the Chairman offered his confirmation of the change)…….One thing is for sure, the markets were certainly not pricing-in a more hawkish stance from the Fed, so it makes total sense that his comments created a big pickup in volatility in many different markets.

Even before he made those comments, the RSI charts on the S&P 500 and the Nasdaq had become quite overbought. By the middle of the month, their MACD charts started to roll-over (even though the S&P remained elevated, and the Nasdaq continued to rally). This was a key sign that the upside momentum for the stock market was losing steam.

Also, the “internals” had deteriorated in a meaningful way in the weeks leading up to Thanksgiving. For instance, even as the market was making new highs in November, the A/D line suddenly rolled over. In fact, in the seven trading days before the market started to roll-over (on November 24th) the NYSE A/D line fell 1.4% (while the S&P and Nasdaq were making new highs). Similarly, when the Nasdaq was making a record high on the Thursday before Thanksgiving, the number of stocks hitting new 52-week lows shot past 400!....We’d also note that the Russell 2000 small-cap index fell 4.5% over the two weeks leading up to November 24th.

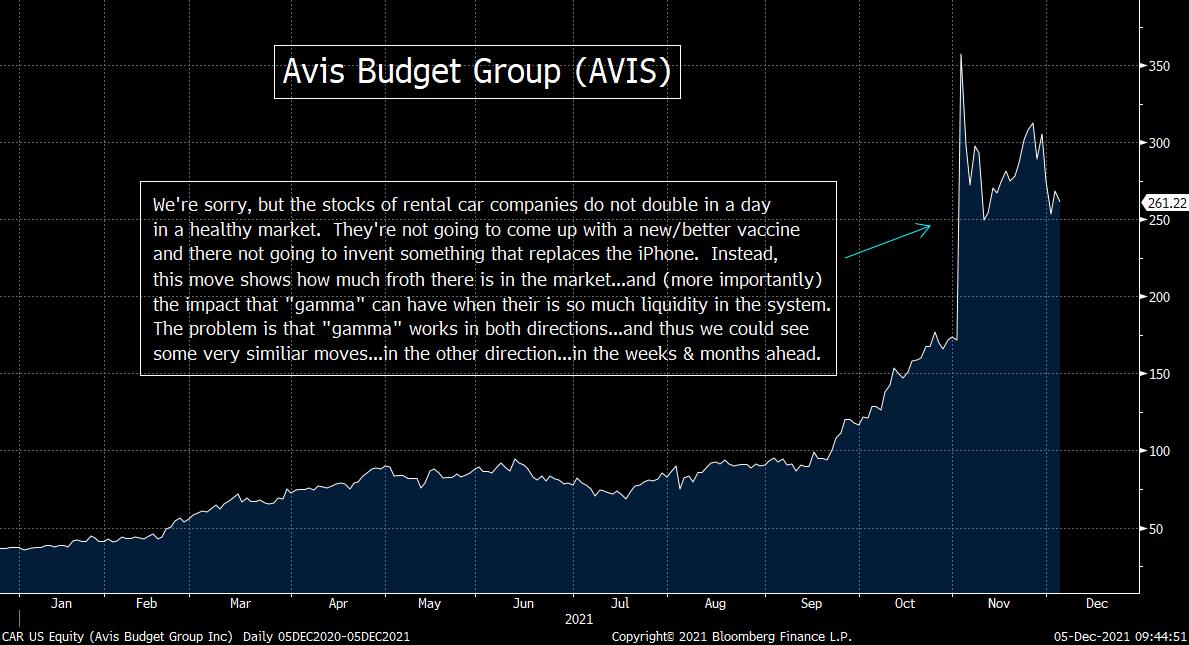

On top of all this, we saw some ridiculous moves in several different stocks. The market cap for RIVN doubled in a matter of days. Avis (CAR) saw its price double in one day! (We’re sorry, but Avis is not going to cure cancer or come up with the next technology innovation. So a 108% rise in one day is an obvious sign of froth in the marketplace.)….We’d even argue that the parabolic rallies in great companies were a sign of froth. NVDA is a great company…with great prospects…but a 56% rally in one month…after it had already rallied 70% in the previous six months…is not the sign of a healthy stock market.

Finally, even though October was filled with a lot of great Q3 earnings reports, the guidance was not anywhere near as positive. In fact, the estimates for Q4…and for 2022…did not move up AT ALL during (or after) the Q3 reporting season. This was MUCH different than the Q1 and Q2 earnings seasons…where earnings estimates rose by 20%. In other words, as good as those earnings reports were for Q3, the “guidance” was showed that the fabulous earnings growth that we had seen all year is beginning to wane.

Therefore, the “set up” going into the last 6-7 weeks of the year was nowhere near as good as those who were looking for a “melt-up” were saying a few weeks ago. Instead (and as we highlighted several times), the only way the market would “melt-up” would be due to even more artificial buying (due to issues like “positive gamma” and “dynamic hedging”). The fundamental and technical set up just wasn’t all that good.

5) Speaking of the impact of “gamma” on the markets, we have also been harping on the fact that “gamma” works in BOTH directions. “Negative gamma” can (and does) also have a big impact on the markets…to the same degree that “positive gamma” can. This is also true for the momentum driven “aglo traders”.

We spent a decent amount of time in recent weeks showing that much of the rally in October was not fueled by positive fundamental news. As we said in the previous point, even though earnings were very strong, they were not strong enough to lead to a rise in future earnings estimates. When you have a market that is extremely expensive, it is very hard to claim that it will rally a lot more…if there isn’t much/any improvement in earnings growth estimates.

Instead, we have highlighted the evidence shows that the impact of “gamma” has been a big help to the stock market in recent months. We can see this by the HUGE level of volume in the call options of the index ETFs…and many of the mega cap tech names. (There was one day where the call options in TSLA were more than 50% of ALL options that traded in the entire marketplace that day!) When investors buy call options, the broker/dealers who sell (write) those options to their customers…have to go out and buy the stock to hedge their positions. When a lot of people buy a lot of call options on a small number of names all at once, it causes the kind of “forced buying” that pushes stocks much higher than their underlying fundamentals would call for…at least any time in the next 12-24 months. (Since a small number of big cap tech stocks have such large weightings in the indexes, it pushed them to artificially high levels as well.)

This issue played a MUCH bigger role in the strong (in some cases, parabolic) rallies that took place in many stocks in October and the first half of November than most people realize. The pundits gave all the credit to the earnings season…because they never want to admit that ANY rally is not fundamentally based. (Of course, they never shy away from blaming many declines on artificial forces…but that’s a story for another time.)

The big problem is that the impact of “gamma’ works in both directions.When all of these call buyers start selling their options and close their positions, the broker/dealers have to sell stocks to close their hedges! This situation can be quickly compounded by new players…who come in and start buying put options in a sizeable fashion…..We saw some of that last week…and will see more of that if the market falls further.

We also have the issue of “momentum based algos.” As certain stocks continued to rally in October/early-November, it caused these algos to buy stocks into a rising market. That, in turn, caused more people to buy call options…which caused more momentum-based buying by the algos…which caused more call buying…and the entire thing fed on itself. However, the exact opposite of that can (and does) take place when the market is moving to the downside. So there is a serious risks involved with these issues going forward.

In other words, if the stock market continues to fall at any time in the coming weeks/months, it is very likely that the decline will get exacerbated by the impact of “gamma” and the momentum based “algos”…just like the rally did in October and the first half of November (in the other direction). Therefore, investors will want to be careful about buying every little dip that comes along. Yes, that worked very well for most of this year, but it might not work as well now that Fed has shifted their policy in a more aggressive way…and that there is still a lot of uncertainly surrounding the omicron variant.

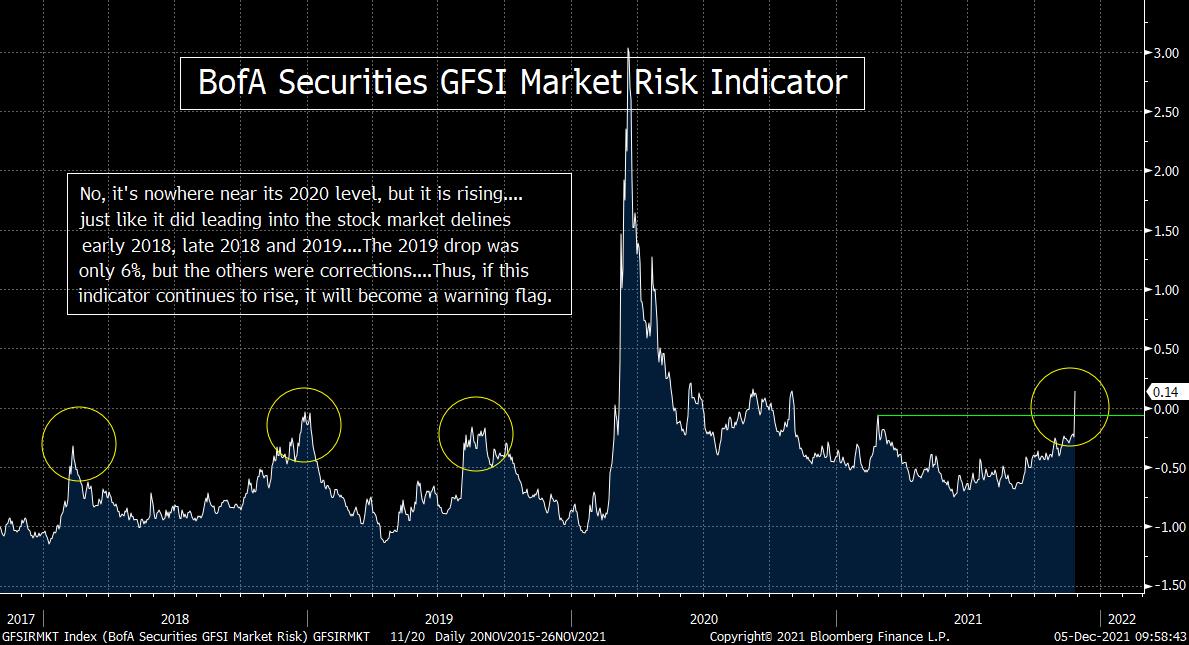

6) Away from the stock market, other markets are also showing some significant cracks. In many of these cases, these cracks did not show up when the stock market has seen other hiccups in the past. This leads us to worry that this more recent decline will become a more meaningful one in the coming months.

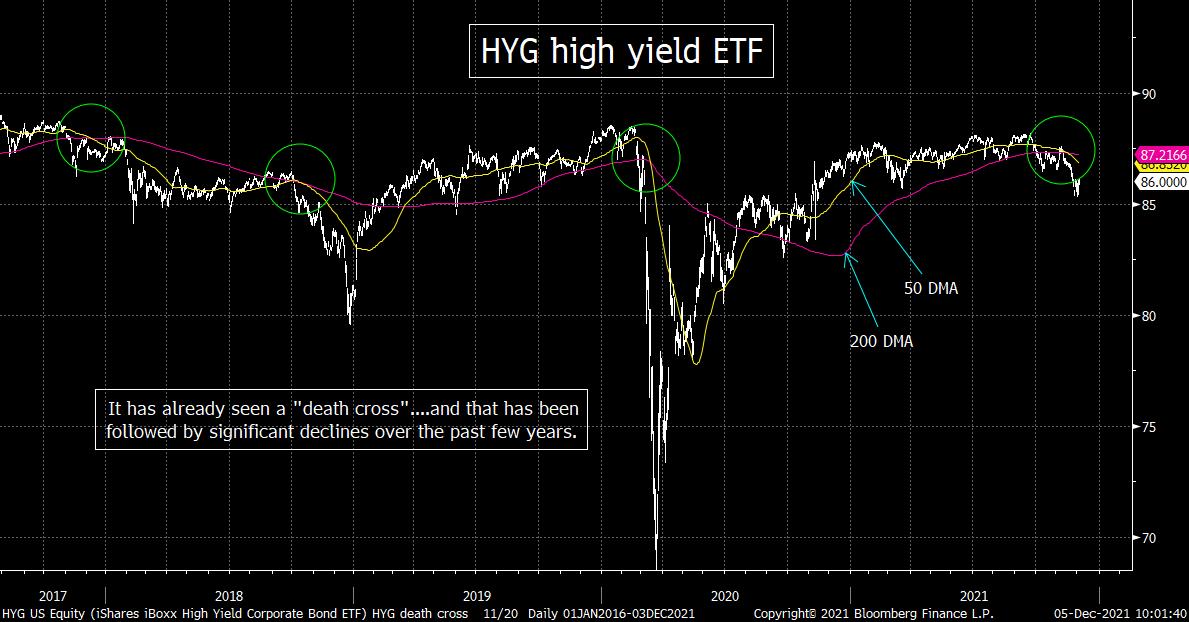

Some compelling cracks are starting to show up in other markets besides the stock market. This is not something we have seen at other times when the stock market has experienced some hiccups since the pandemic lows. For instance, the Citi Macro Risk Index is shooting higher…the HYG high yield ETF has dropped…and CDS (insurance) prices for high yield bonds are rising. This could be telling us that this decline in the stock market is not going to be as short-lived as so many others have been this year.

The Citi Macro Risk Index looks at credit spreads, swap spreads and implied volatility for several major asset classes…and it is seen as a good indictor for risk aversion in the global marketplace. This number has actually been moving higher since this past June. Therefore, its rise has not been solely due to concerns over the omicron variant or the recent more hawkish comments out of the Fed. It has ben rising for almost six months! There is no question that it has moved in a more significant way over the past few weeks, but its multi-month advance shows that risk aversion in some areas of the marketplace has not been a very recent phenomenon.

As for the high yield market, the CDS prices (which is the price it costs to insure against default for those bonds) have risen significantly. We do admit that they’re still well below their March 2020 lows (when it looked like the high yield market would completely freeze-up), but these prices have risen to their highest level of the year.

The HYG high yield ETF has seen a meaningful drop as well. It has fallen well below the sideways trend it had been in since last spring…and this had given it a “death cross” during November. “Death crosses” have been very negative developments for the HYG in years past, so this is not good at all. Some traders liked the fact that the HYG did not move much at all on Friday. However, this ETF had become quite oversold late in November, so its better-than-expected action late last week looks like it was merely something that was working off its oversold condition. Therefore, we’ll be watching to see if this decline resumes…at some point next week…now that some of that oversold condition has been worked-off.

The point is that some of the cracks we’re seeing in the marketplace are not isolated to the stock market. That does not mean that the stock market will definitely decline a lot further immediately. However, it does not bode well for risk assets over the coming months.

7) As many people watch the dollar closely much of the time, the most important move in the currency market last week came from the euro/yen cross. This is a very important indicator for the “carry trade”…and thus it’s an important indicator for the level of excess liquidity in the system. Therefore, if the euro/yen continues to decline, it will be a bearish development.

Most people here in the U.S. keep a close eye on the level of the dollar on a regular basis. However, many of us also watch other currencies. For instance, the euro is a key currency…as it tends to be a good indicator for the “risk-on” trade. Japan’s yen is another one…as it tends to be a good indictor for the “risk-off” trade. Therefore, by watching the euro/yen cross, investors can get a good idea of the risk-on/risk-off equation for the broad marketplace.

Another reason to watch the euro/yen cross is that it is a very good indicator for the “carry trade.” This is important because the “carry trade” tends to be a good indicator for the level of liquidity in the system at any given time…….The problem right now is that the euro/yen broke below a key support level late last week. The 128 level has been support in recent months and it broke below that level late last week. That said, it only broke it by a very small amount. Therefore, it could bounce back quickly…and ease everybody’s concerns rather quickly.

However, it has already broken below its 200-DMA…and below its trend-line from the spring 2020 lows…so if it does fall further, it will confirm a change in trend for the euro/yen cross…and that would not be a good sign for the level of liquidity in the system as we move towards the end of 2021. THAT will not be good for those looking for a big “risk-on” move into year-end (and beyond).

8) Let’s look at the technical condition of the stock market. Although it seems like the market has gotten clobbered, it’s not down all that much at all…and it hasn’t experienced any significant technical damage. We’ll explore the key support/resistance levels for the S&P 500, the Nasdaq and the Russell 2000 in this bullet point.

There is no question that we’ve see a BIG pickup in volatility since Thanksgiving…as the stock market has seen several wild swings in both directions. This has pushed the VIX volatility index above 30 and sent a certain amount of fear into the marketplace. However, the S&P 500 is only 3.5% below its all-time highs. That’s a TINY decline…and not even as much as the September swoon of 5% gave us. For the Nasdaq, it stands just 6% lower…which is also a smaller decline than we saw two months ago. Yes, the Russell 2000 fallen more than 11%, so we don’t want to try to say that there has been zero technical damage in the stock market recently. However, since the Russell had been underperforming all ye

Recent free content from Matt Maley

-

THE WEEKLY TOP 10

— 10/23/22

THE WEEKLY TOP 10

— 10/23/22

-

Morning Comment: Can the Treasury market actually give the stock market some relief soon?

— 10/21/22

-

What Do 2022 and 1987 Have in Common?

— 10/19/22

-

Morning Comment: Which is it? Is stimulus bullish or bearish for the stock market?

— 10/17/22

-

Morning Comment: Peak Inflation is Becoming a Process Instead of a Turning Point

— 10/13/22

-

{[comment.author.username]} {[comment.author.username]} — Marketfy Staff — Maven — Member

- 1 Campus Martius, Suite #200Detroit, MI 48226

- +1 877 440 9464