THE WEEKLY TOP 10

We’d like to highlight something we haven’t mentioned in a while. In our weekly update each week, we frequently highlight issues that are in in direct conflict with one another. In other words, we sight things from both sides of the bull/bear ledger…and thus it may seem like we’re talking out of both sides of our mouth. What we’re really trying to do is to highlight issues from both sides of the ledger…while still letting you know which side of the ledger we stand on at any given time. Thank you very much.

THE WEEKLY TOP 10

Table of Contents:

1) China, U.S., & Europe: All becoming less accommodative. That’s bearish.

2) 1.6% on the 10yr yield is not low enough to justify a 21x multiple.

3) S&P 500 breaking out? Can it accelerate even further into year-end?

4) The healthcare sector has a lot of upside potential going forward.

5) Tech earnings are important, but don’t ignore the others.

6) Several technical reasons to think LT yields will continue to rise.

7) It didn’t take long for the froth in the marketplace to resurface.

7a) Bitcoin taking a breather…not a big problem.

8) Keep a close eye on the XLI industrial stock ETF.

9) The bounce in the high yield market didn’t last very long.

10) Summary of our current stance.

1) As we will discuss in point #2, there is no question that last week was a good week for the stock market on a technical basis. However, we still believe that an important change has taken place in China…and an important change is about to take place in the U.S. and Europe. All of these changes will cause the use of leverage to decline…and that will cause today’s very expensive stock market to correct before long.

We have highlighted several times in recent weeks that it is our belief that the most important development for the markets and the economy in 2021 around the globe has been the major change that China has gone through. They have gone from encouraging companies and investors to take-on massive risk, massive debt and leverage (for MANY,MANY years)…to a situation where they are causing (forcing) their companies and people to de-leverage and de-risk themselves in a significant way.

We don’t want to bore you by repeating evidence that shows this major de-risking/de-leveraging play…except to say that it started with Jack Ma a year ago…and it has spread to many other groups/sectors of their economy over the past 12 months…..Evergrande is not going to “cause” anything. It’s the change in policy that “caused” the problems at Evergrande…and to think that the real estate industry is the only one that was leveraged enough to eventually run into serious problems is ridiculous. Evergrande was not a “Lehman moment” because those “moments” don’t come at the beginning of a de-leveraging cycle, they come near the end of one. (Besides, we don’t HAVE to have a “Lehman moment” to prove the situation is a tough one. Thirty years ago, Japan embarked on a serious de-risking/de-leveraging policy…and it did not create a major crisis. It “only” led to a lost decade.)

We also have a situation where the Fed and the ECB are about to start tapering back on their MASSIVE QE programs very soon…maybe as early as mid-November. Right now, the Fed is buying $120 billion of bonds every month. This is going to go to zero within 6-8 months (or even quicker if some members of the FOMC get their way).

In other words, we are moving from a situation where an historic level of stimulus is being pushed into the system (and thus pushed the markets to artificially high levels)…to one where a lot less stimulus will be available. This will leave the stock market to trade on its own. That would be fine if the S&P 500 was trading at 15x forward earnings…like it was the last time they tapered back on a big QE program. Instead, the market is trading at 20.5x forward earnings. Therefore, it’s going to be VERY DIFFICULT for the stock market to rally a lot as we move into early and mid-2022.

In fact, we think it will have to come down in order to trade more in line with the fundamentals of the companies in the S&P 500. With the emergency level of stimulus going to zero in just a few short months, the stock market will find it very difficult staying at its current level in our opinion.

2) We disagree with those who argue that the low level of long-term interest rates justify today’s elevated valuations…and we disagree with those that the level of liquidity (after the Fed begins to taper) will still be strong enough to push stocks higher over the next 6-12 months.

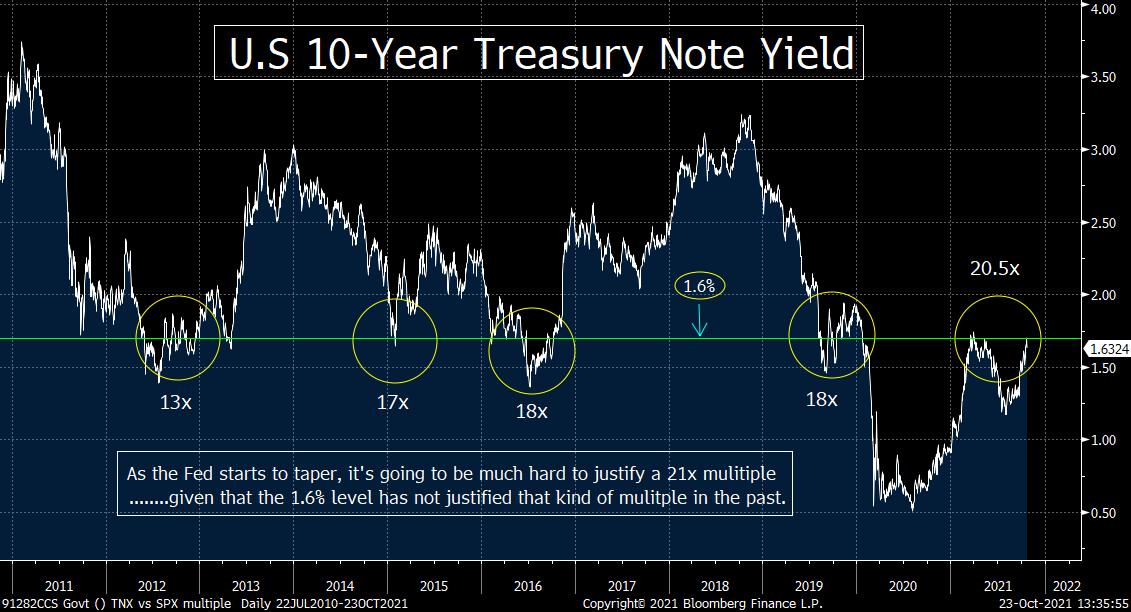

We want to reiterate our stance that we do not believe that today’s low level of long-term interest rates is something that justifies the extremely elevated multiple for the stock market. Don’t get us wrong, interest rates certainly ARE low on an historical basis. However, we’re a long way from the 0.5% level we saw in mid-2020…which is the only time long-term yields were ever that low. The U.S. 10-year yield is now well above 1.6%. This is not a unique level. The 10yr yield has been at the 1.6% level four other times in the last decade.

On those four occasions, the stock market did not trade anywhere near the 21x multiple it’s trading at right now. As the chart below shows, the last four times the 10yr yield stood at 1.6%, the multiple on the stock market was 13x, 17x, 18x, and 18x respectively. In order for the S&P to be trading at the highest level of those examples (18x), it would have to fall below 4,000! (Chart attached below.)

Many pundits simply throw-out the excuse long-term rates are low and thus the market’s high multiple is fair, but they never tell us what the correct “fair value” is for any given level of interest rates. If they used history, they would have to admit that the stock market is very expensive and thus well ahead of its fundamentals…and that it was merely the emergency level of liquidity that has kept the market well ahead of those fundamentals (which everybody would admit was the case in the summer of 2020). Now that much of this stimulus is going to disappear, it’s going to be MUCH harder to justify today’s valuation.

As for the thought that we’re still going to have plenty of stimulus after the Fed tapers, we think this is an empty argument as well. The Fed is going to go pumping $120 billion PER MONTH…to zero…in a matter of 6-8 months (and maybe even quicker)…..It’s great that they’ll still be pumping a decent amount in during the month of January, but when the system is used to getting $120 billion per month, a significant drop-off will still have an impact. In other words, we readily admit that they’ll still be buying $800-$900bn of securities in January…like they were during the first half of 2011…but the stock market was trading at 14x forward earnings back then!!!

The situation is like a weightlifter who takes steroids. He’s strong on his own, but he gets even stronger through the use of artificial stimulants (steroids). If he starts to “taper” back on his steroid use, it won’t matter if he’s still taking SOME steroids…he will still lose some of his strength and he won’t be able to lift as much weight without the full allotment of the steroids. By the time he lowers his steroid use down to zero, he’ll STILL be strong. He will still be able to lift a lot of weight. However, his performance will still progressively move to a lower level as he tapers back on his steroid use. Once his performance gets down to the level that works with his own natural muscles (and no artificial help), his performance will level off. Then it will rise of fall on his own natural abilities.

This is what’s going to happen to the stock market in our opinion. This is especially true given that the market is a forward-looking instrument. It looks out 6-8 months. Well, guess what? Six to eight months from now, the stock market will have to act on zero steroids (QE). How is it going to stay at 21x earnings…especially since 1.6% does not justify that kind of valuation?

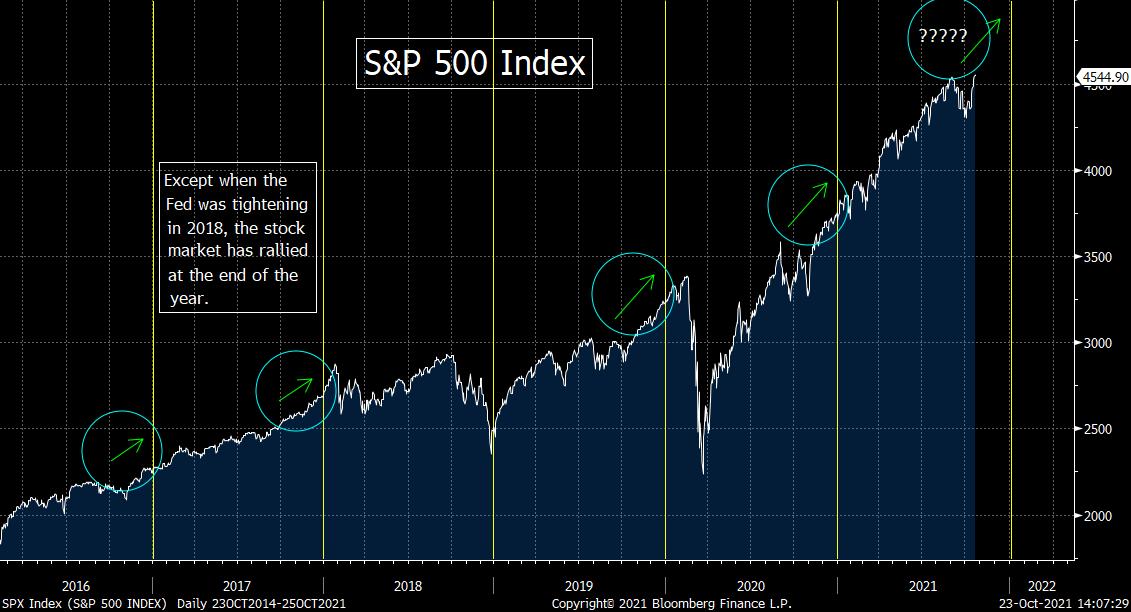

3) The confirmed break above the 50-DMA on the S&P 500 (and the Nasdaq) is certainly a bullish development. This is particularly true given that we’re heading into the last two months of the year. As that happens, institutional investors (even the ones who claim they are only interested in the long-term) become very focused on the short-term. This could create a surprising rally at the end of the year.

As we have been saying, the 50-DMA had been “old support” and thus it became the “new resistance” for the stock market…and both the S&P 500 and the Nasdaq broke back above this key line last week. Therefore, this is definitely a bullish development. This could become an even bigger development if these indices continue to rally once we get very far into the month of November.

The reason for this is because ALL investors become short-term oriented. This is especially true for institutional investors (even the ones who claim that they only look at the long-term). This has to do with performance fear. No, we’re not talking about the kind of performance fear that can be cured for some people with Viagra. We’re talking about the performance of their portfolio.

Portfolio managers whose performance is lagging are particularly sensitive to how the market behaves at the end of the year. Their job security could depend on it. The absolute last thing they can do is fall further behind the market at the end of the year…….However, it’s also important for those who are ahead of the market…even well ahead of it. Their bonus will depend on how they stand at the end of the year. So, they always want to maintain their lead…and even grow it…as they go through the last 6-8 weeks of the year.

Therefore, these institutional investors will focus on two areas. (We’ll talk about the first one here…and then discuss the second one in the next bullet point.) The first area they focus on is the stocks that have the most momentum. Needless to say, the stocks with the most momentum at any given time always do well (at least for a while). However, the ones that are “working” tend to do even better late in the year.

Unless a portfolio manager is WAY ahead of his/her bogey, they do not spend the end of the year setting up their portfolio for the next year. (They do that early in the new year.)……They do what they can to make sure that they keep their lead…or even extend it (or catch-up, if their behind). Sure…in May, June, or July, they would allocate a decent amount of money into some other longer-term ideas. However, at the end of the year, they won’t allocate much money to those stocks…if they think those names won’t work in a significant way for several months. They’ll focus any new inflows into the stocks that are rallying.

If the market has had a good year, the institutions investors concentrate their buying power on the stocks that have been working. Since those are the names that have already pushed the market higher for most of the year, the concentration of flows tends to push it even higher at the end of the year…and the whole thing feeds on itself. In other words, there’s a good reason why we tend to see a year-end rally most years.

4) There is sometimes another year-end trend. For those institutional investors who need to play catch-up (or want to gain on their winning performance vs. their bogey)…they look at groups that HAD been lagging most of the year…but have turned higher late in the year. Of course, there are many years where no group falls into this category. However, when it does take place, it can have an outsized impact on the group in the last few months of the year. Right now, the healthcare sector looks intriguing on this front.

As we said above, institutional investor tend to focus on the hot stocks going into the end of the year. However, they also focus on stocks and groups that gain momentum late in the year as well. Grabbing these stocks late in the year can help an institutional investor play catch-up if they’re behind their bogey (especially if the group has a low weighting in their bogey). It can also help those who want to get further ahead for those who are beating their bogeys. (The first part of that is for job security, the second half is for a better bonus.)

Let’s face it, whenever a stock or a group has been underperforming for a while, they tend to do very well once the worm finally turns. “New momentum” always attracts money…and the rally can frequently get an extra boost from short covering. (Needless to say, groups that have been underperforming for a while tend to build a decent amount of short interest.) Therefore, this tends to attract a lot of interest from institutional investors who are trying to play catch-up.

If they become overweighted in group that is underweighted by their competition and is suddenly outperforming the market, it can help one’s performance……It is VERY difficult for a manager to play catch-up late in the year, but this is one way that they can definitely make up some room.

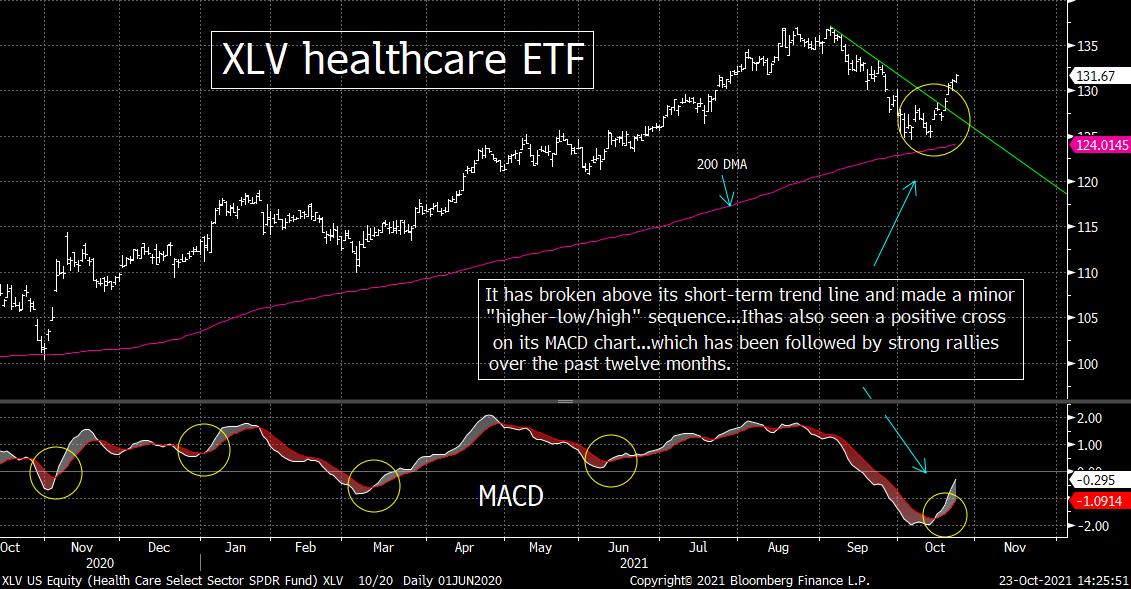

With this in mind, we’d like to focus on the healthcare sector this weekend. We touched on the upside potential for the biotech group recently, but the broad healthcare sector is also starting to show some promise. The XLV healthcare ETF became very oversold at the beginning of this month. It tested the $125 level several times (and held)…and now it starting to bounce off that level (which is just above its 200-DMA). The bounce over the past couple of weeks has given it a minor “higher-low/higher-high” sequence…AND it has also taken the XLV above its short-term trend-line from early September…so this is a positive development.

It’s a little too early to send a major green flag up the flag pole, but there is no question that if it can see a bit more upside follow-through, it’s going to be very bullish for the healthcare sector as we move towards the end of the year. This is especially true given that the XLV is seeing a positive cross on its MACD chart. As you can see from the chart below, every time the XLV has seen a positive cross on its MACD chart over the past year, it has been followed by a strong rally in this sector. Therefore, if we get any upside follow-through, this sector should be one that does VERY well over the last 2.5 months of this year.

As for a specific stock in the group, AMGN is looking quite good on the charts. It is bouncing off an oversold condition on both its daily and weekly RSI charts…and its MACD chart just made a positive cross. Most importantly, AMGN has fallen slightly below its 200-week moving average. It has fallen slightly below that line on four other occasions in the past decade…and each time it was able to regain that line rather quickly. Not only this, but the rally that followed was swift to start…and then gathered some meaningful longer-term momentum as well.

AMGN bounced back last week and is now very close to testing that 200-week MA. (Again, we’re talking about the 200-week MA, not the 200 day MA.)…..If it can break above that line, it could/should regain the kind of upside momentum that will give it a very strong rally leg into the end of the year…and beyond.

5) As usual, the vast majority of companies are beating their earnings estimates so far. However, we definitely saw some cracks in the “forward guidance” from several companies last week. Therefore, even though most investors will be focused on the big cap tech earnings releases next week, we’ll also be watching the guidance from many other sectors as well.

This earnings season has been a good one so far…as about 84% of the companies reporting are beating expectations on earnings…and almost 75% are beating on sales. However, as we all know, the majority of companies in the S&P 500 always beat their estimates. Thus, we always look for any positive or negative trends on the “forward guidance” that is provided by these companies. This will be especially important this time around…because everybody wants to know whether the supply chain issues, the rise in commodity prices, and wage issues are going to continue to create problems for earnings growth in Q4 of this year…and in the first half of 2022.

Next week, most of the focus will be on the earnings from several big tech companies….as Facebook (FB), Alphabet (GOOGL), Microsoft (MSFT), Amazon AMZN), and Apple (AAPL) all report. Needless to say, we totally agree that these earnings will be very important for the techs sector…and for the market as a whole. The tech sector was a key leadership group during the summer months, so whether it can continue to rally or not should be important for the entire stock market. This is especially true given that long-term interest rates are rising. In other words, it will be important that the sector has something to offset the renewed headwind that is being created by higher yields.

However, we will also be watching many other groups. The main reason for this is that we definitely heard some “guidance” last week that was not very bullish at all. Companies like Honeywell (HON), VF Corp (VFC), Proctor & Gamble (PG), Brinkers (EAT), Oshkosh (OSK), US Xpress (USX), and Nucor (NUE)…all gave disappointing guidance. They all sighted raw material inflation, or labor market challenges, or supply chain issues (or all three) as reasons for lowering their guidance. Therefore, it isn’t a big surprise to see that earnings forecasts for future quarters/years have not gone up at all so far this earnings season.

Of course, it’s still early in the earning season, so things could change for the better. However, if this “flow” of lower guidance becomes strong/steadier “stream” of lower guidance, it could easily lead to a lowering of Q4 and 2022 consensus earnings estimates. Any lowering of estimates will obviously make the stock market even more expensive…….Given that the S&P 500 is already trading with a multiple of almost 21x, that will not be a bullish development…with inflation and long-term interest rates on the rise.

Therefore, even though we will certainly be watching those very important big cap tech earnings, we’ll also be following the rest of those earnings reports/guidance. Given how expensive the market has become again, it won’t take much of a fall in earnings estimates in the coming weeks for it to create headwinds for the broad stock market.

6) The yield on the U.S. 10-year note rose once again last week and now stands within striking distance of its March highs of 1.75%. Given that the German 10-year bund has already broken above its own March highs and the U.S. 10yr yield is about to see a golden cross, it looks like the 2021 highs for long-term interest rates in the U.S. could be exceeded a lot sooner than most people think.

The yield on the U.S. 10-year note rose again last week…which makes eight of the past nine weeks. Since its early Augusts lows, the 10yr yield has bounced from the 1.1% level to 1.63%...and this has involved a series of minor “higher-lows/higher-highs.” (We’d also note that the 10yr yield made a major “higher-low” this summer…at a much higher level than the 2020 lows.) Therefore, if it can break above its March highs of 1.75% (and follow that major “higher-low” with a major “higher-high”), it’s going to be a very compelling development. It will confirm beyond a shadow of a doubt that the trend for long-term interest rates is an upward one. (First chart below.)

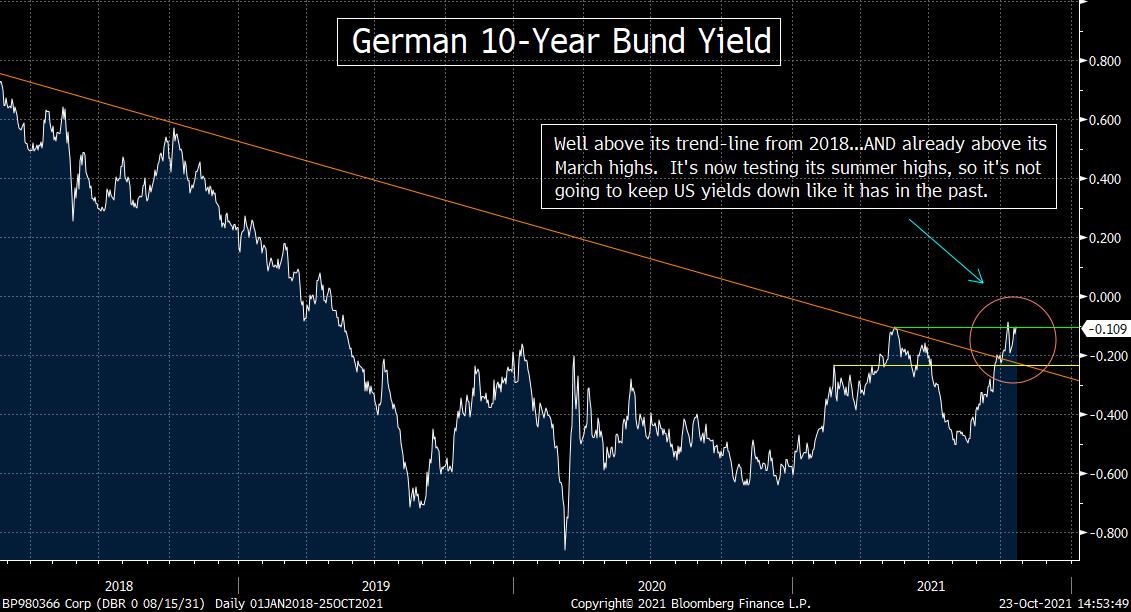

Given that we continue to see more and more signs that inflation will be with us for a long time, its starting to look like those long-term yields will indeed continue to rise…and break above those spring highs. However, there are some other reasons to think this could happen. First, the yield on the German 10-year bund is already broken well above its own March highs…and is now testing their summer highs!

Remember when everybody said that U.S. rates could not rise very far because European/German yields remained so low? We’ll those yields are now at 2-year highs…and if they keep on rising, it will only be a matter of time before U.S. yield break to new highs as well. (Second chart below.)

We’d also note that the chart on the 10yr yield shows that it is getting very close to a “golden cross” (where its rising 50-DMA crosses above its rising 200-DMA). As the third chart shows below, the 10yr yield has seen several “golden crosses” in the last decade. All of them were followed by further rises in interest rates…and the last three were followed by substantial rises.

Finally, we would add that a rise above the March highs would mean that the 10yr yield had made a new 52 week high. The last time that happened was in Q4 of 2018…just as a deep 19% correction in the stock market was unfolding.

7) A few weeks ago, when the stock market had fallen a mere 5%, investors had quickly turned quite bearish on the stock market…and the meme stocks and SPAC shares has stopped going up. In other words, sentiment was no longer exuberant and a lot of the froth in the market had disappeared. Well, that has changed back very quickly.

When the stock market was trading down by about 5% at the beginning of this month, we said that the one thing that concerned us most about our cautious stance was that too many other people were also cautious. Well, that has changed quite quickly. No, the numbers have not jumped to extreme levels…and the Investors Intelligence data has not moved as much as some of the others. However, there is no question that bullishness has still made a big comeback. In the AAII poll of individual investors, the bulls have jump over 21% over the past two weeks to over 45%. In the DSI data, it shows that bullishness among futures traders jumped into the mid-80s last week for both the S&P 500 and the Nasdaq. (It will also be interesting to see where the II and AAII numbers come-in next week…when the include the rise to a new all-time high for the S&P 500.)

The meme stocks and the SPACS have come roaring back as well. We all heard about the SPAC linked to Donald Trump’s social media venture (DWAC) which rallied over 1,600% at its highest-level last week. However, several meme stocks…like Phunware (PHUN), Anthem (ANTM), Upstart (UPST), Vinco Ventures (BBIG), Macy’s (M), etc…have all seen meteoric rises in the last week or two…none of which can be fully explained by any new fundamental news.

Of course, we have also had the big rally of over 60% in Bitcoin in the past three weeks. Now, we readily admit that there has been some very good news out in the crypto asset class (with their new ETF), but most of that rally took place before it became evident that the SEC was going to allow these crypto ETFs. In fact, most of the new until very recently should have weighed on Bitcoin (China’s decision to outlaw trading…and Gensler’s warnings about regulation). So there’s little question that the speculative juices have been flowing in this area recently as well.

Again, we don’t want to imply that these developments have moved to huge extremes. (Sentiment has become more bullish, but it’s not extreme. Meme stocks are rallying, but not as many as we saw over the summer. Bitcoin’s rally has been extraordinary, but there definitely was some positive news.)

However, Mr. Market has a way of burning everybody when a deep correction takes place. This most recent rally has caused some bears to flip and become much more bullish…and it has turned those who were merely “concerned” into outright bulls again. In other words, this just might be a situation where certain players have just “covered” their bearish bets…just before the real decline takes place.

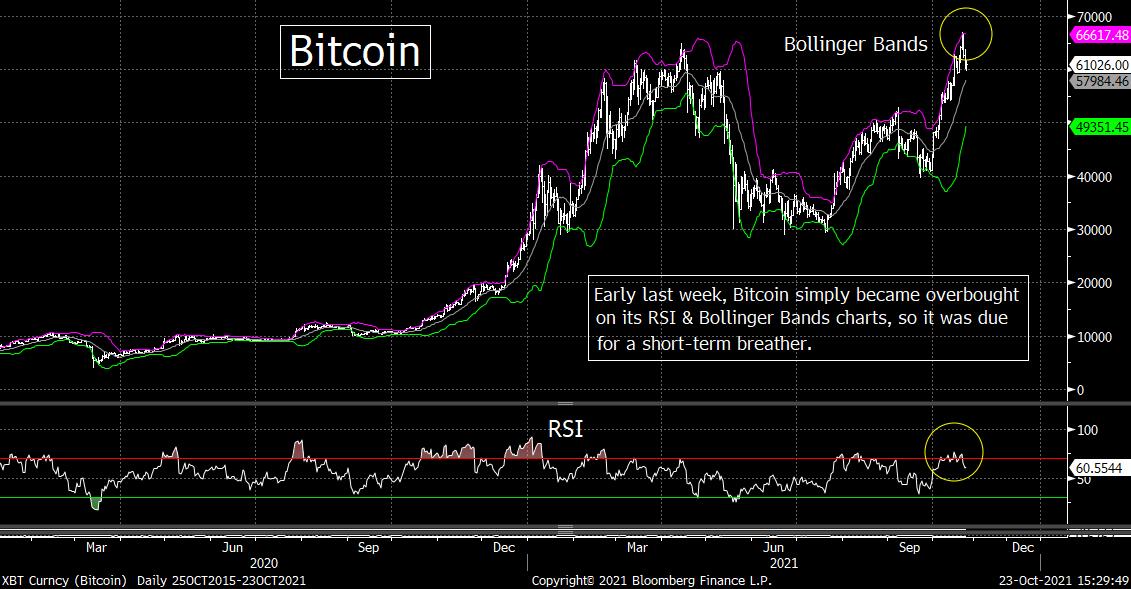

7a) We do not want to imply that we think Bitcoin or other cryptocurrencies have moved too far or that they’re going to crash at some point soon. We’re merely saying that a 50% rally in only 4-5 weeks…even for something like Bitcoin…is a sign that the speculative juices are strong right now…….In fact, we remain bullish on this asset class on a longer-term basis.

We do not want to imply that we think Bitcoin or other cryptocurrencies have moved too far or that they’re going to crash at some point soon. We’re merely saying that a 50% rally in only 4-5 weeks…even for something like Bitcoin…is a sign that the speculative juices are strong right now…….In fact, we remain bullish on this asset class on a longer-term basis. We think last week’s pullback was merely something that worked-off a short-term overbought condition. After a 50% gain, it had become quite extended on both its RSI chart and its Bollinger Bands chart…so it had become ripe for a breather.

This breather could last a bit longer. It could even give back 50% of its most recent rally (like it did in late September). That would take Bitcoin down below $54,000, but the chart on Bitcoin looks great and we would expect “higher-highs” before long.

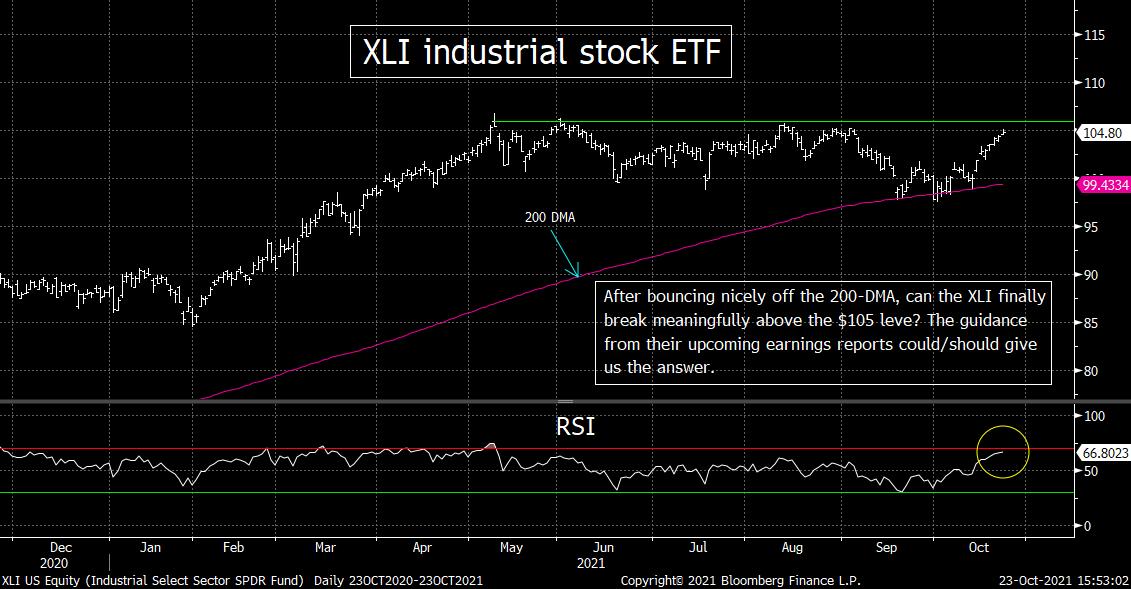

8) As we highlighted in point #3, the earnings guidance from many different groups is going to be important. The focus will indeed be on the tech group, but we’ll also be looking at the industrials. They could be particularly susceptible to the problems with the supply chain…as well as commodity and wage price issues. The XLI is close to a very important resistance level. Whether it breaks that line…or rolls back over in a significant way…could/should be very important for the broad stock market.

In point #3, we highlighted how several companies have lowered their earnings guidance going forward. We know that many of the industrial companies are quite vulnerable to the supply chain problems, higher commodity costs, and wage issues. Therefore, the guidance they provide as they report over the next few weeks should be quite important.

Looking at the chart of the XLI industrial stock ETF, it looks quite good. However, it’s going to have to see a bit more upside follow-through in order for us to raise a big green flag on the sector. The XLI bounded off its 200 DMA three different times recently, so that is certainly positive. Now, it is pushing up toward the $105 level. That price has provided VERY tough resistance for the XLI for six months now. (Actually, the resistance level is slightly above $105.) It bumped up against it in May, June, August, and September. In other words, if it fails to break above that level once again, it’s going to be quite negative. However, if it can finally break above $105 in any meaningful way, it’s going to be very bullish.

What we’re saying is that the industrial stocks stand at a key technical juncture. Thus, how the XLI acts as these companies report their earnings over the next couple of weeks should be quite important. It should also be important for the broad market as well. It should tell us just how much of a problem the supply chain issues…and inflation…will (or will not) be over the next six months or more. The broad stock market is telling us right now that they won’t be as big of a problem as some pundits fear, but we’ll have to see what these industrial companies have to say about these issues over the next week or two.

9) The high yield market bounced back in the middle of this month, but it’s starting to see some signs that it was merely a dead cat bounce. If (repeat, IF) we see this market roll-over to a lower-low (and its spreads widen out to a “wider-wide”), it’s going to raise an important warning flag on the markets in general.

We thought it was very interesting that the strong 2-3 day bounce in t

Recent free content from Matt Maley

-

THE WEEKLY TOP 10

— 10/23/22

THE WEEKLY TOP 10

— 10/23/22

-

Morning Comment: Can the Treasury market actually give the stock market some relief soon?

— 10/21/22

-

What Do 2022 and 1987 Have in Common?

— 10/19/22

-

Morning Comment: Which is it? Is stimulus bullish or bearish for the stock market?

— 10/17/22

-

Morning Comment: Peak Inflation is Becoming a Process Instead of a Turning Point

— 10/13/22

-

{[comment.author.username]} {[comment.author.username]} — Marketfy Staff — Maven — Member

- 1 Campus Martius, Suite #200Detroit, MI 48226

- +1 877 440 9464