THE WEEKLY TOP 10

THE WEEKLY TOP 10

Table of Contents:

1) If the S&P, Nasdaq & Russell can see meaningful breakouts, we’ll have to turn more constructive.

2) Despite the way it seems, the stock market rally has stalled-out.

3) There are signs that the drop in bond yields will end soon.

4) Even if inflation does not become a big problem, LT rates are going to rise.

5) The supply/demand equation is much more important…and its changing.

5a) Don’t listen to the Fed when they say the end of SMCCF is not a “taper” move.

6) European stocks are getting overbought and are now due for a “breather.”

7) What’s wrong with Taiwan Semiconductor?

8) Natural gas is getting overbought on a near-term basis.

9) The battle lines are well drawn for Bitcoin. (Is that important for other assets?)

10) Summary of our current stance.

1) There are many reasons to think that the stock market cannot rally a lot further from current levels. Several of which we’ll cover this weekend. However, with the S&P 500 Index closing at a new all-time highs and the yield on the U.S. 10-Year note breaking below the bottom end of its recent range, the outlooks for the stock market over the near-term looks quite rosy. Therefore, IF (repeat, IF) we see the S&P 500 index breakout in a more meaningful fashion…AND we see confirming breakouts in the Nasdaq and Russell 2000…we’ll have to turn much more constructive on the stock market for the summer.

The S&P 500 closed at a new all-time high once again on Friday, so this is obviously a positive development. We’d also note that the Nasdaq Composite is only 0.5% away from its record high and the Russell 2000 is only 1% away. Of course the new high in the S&P is only a slight one so far, so it…and the other indices will have to make more meaningful upside moves to confirm that a breakout is taking place, but the potential is definitely there.

We have also seen a significant downside break of the multi-month yield on the 10-year note. It closed at 1.46% on Friday…which is qualifies as a “meaningful” break of the lower line of that sideways range (which stood at 1.53%). One of our biggest concerns about the stock market has been that the yield on the 10yr note would see another upside leg…and that this would cause problems for the stock market on several fronts. It would create headwinds for the tech stocks and it would force some of the massive levels of leverage that exist in the system today to be unwound. Since those long-term rate have moved in the other direction, it is certainly a bullish development.

What we’re saying is that we HAVE TO AVOID being stubborn about our cautious stance. Just because we think that long-term rates SHOULD move higher soon…and thus the stock market SHOULD correct soon…we will HAVE to change out stance if we get confirmation of the breakout in those all-important three stock indices.

2) Having said all this, it is surprising that the stock market has not acted better over the past couple of weeks. The decline in long-term rates has been a significant move and yet the S&P is only slightly higher than it was two months ago. Also, the Russell is actually slightly below the level it was three months ago and the same is true for the Nasdaq going back four months! Therefore, if (repeat, IF) long-term rates bounce-back in a substantial way over the summer, these indices could/should get slapped upside the head.

Even though the S&P 500 has made several new record highs since April, it only stands 0.35% above its May highs and just 0.85% above tis April highs. Looking at the Nasdaq, it still stands slightly BELOW its highs from both February and April…and the Russell 2000 closed 1% below its March highs on Friday. In other words, the S&P 500 has done very little over the past two months…and the same can be said about the Nasdaq and the Russell over the past 4 months and 3 months respectively.

From February to April, we saw Bitcoin double and Ethereum do even better (jumping over 200%)! We have also seen some commodities (like lumber) double over just a six-week period at one point this spring. Similarly, we have seen “meme stocks” like AMC jump over 400% and CLOV climb over 200% during May and June. (On top of all this, homes are being sold for tens of thousands of dollars over the asking price…sometimes hundreds of thousands more.)

In other words, some incredible rallies in a small number of different asset classes have made it SEEM like the stock market (in general) has been on a huge upward trajectory in recent months…when it actually has not done much at all. Given that the yield on the 10yr note has fallen from 1.75% to 1.46% since late March, this is not the kind of action that says the stock market is going to rise a lot further going forward.

Don’t get us wrong, the inability of the stock market to rally a lot further in the face of a significant drop in interest rates is not negative in-and-by-itself. This could merely be an extended “breather” before the stock market moves higher. However, as we will explain below, there are reasons to believe that the end of the decline in interest rates might be just around the corner. Thus, if the stock market could not rally much when rates were falling, we wonder what will it do if those rates begin to bounce-back in a serious manner.

3) There are two items on the technical side of things that could throw a wrench into the bullish picture that many pundits have been pushing over the past week or two when it comes to interest rates. If we are right about these technical issues, the yield on the 10yr note could/should be bouncing back very quickly… and quite soon.

We heard a lot of talk last week that the action in the Treasury market is telling us that the strong-than-expected inflation data will be transient…just like the Fed has been saying it will be this year. The Fed could certainly be correct. However, we believe that the more likely outcome is that although inflation could/should pull-back from whatever highs it sees over the coming months, it will plateau at a much higher level than we have seen for several decades.

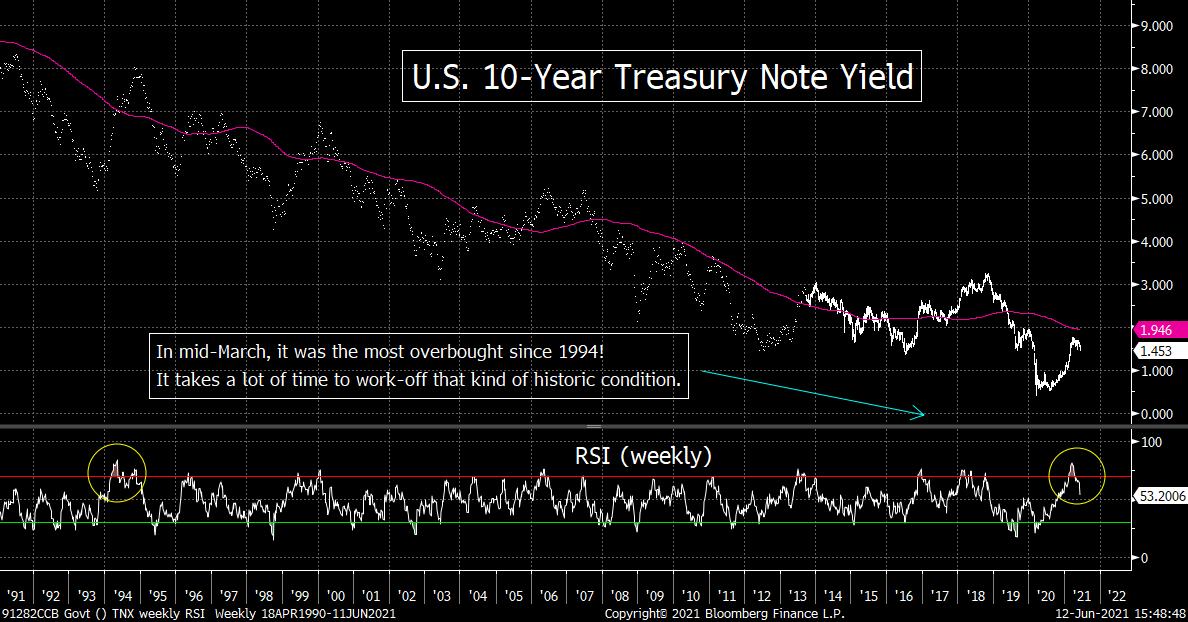

Either way, we can certainly make an argument that the decline in interest rates that has taken place since late March/early April is merely a technical reaction to the extreme oversold condition that the Treasury market faced at that time on an intermediate-term basis. (Extremely overbought in terms of interest rates.)

If you’ll remember from our notes when the TLT Treasury ETF (which measures prices) was reaching its spring lows and the 10yr yield was reaching its spring highs, we highlighted that the weekly RSI chart on the TLT had become the most oversold it had EVER been since its inception in 2002! Similarly, the yield on the 10yr note had reached its most overbought condition on its weekly RSI chart since the early/mid-1990s!!!! These are not the kinds of readings that can be worked-off in a matter of days or weeks. It takes several months for this to take place. Therefore, the most recent drop in yields could be something that is merely a part of the process to work-off those extreme technical conditions.

The question is; when will this process end? If the decline in yields has merely been a technical move, when will it end? Well, it could be quite soon because we are seeing some signs that the TLT is topping out and that long-term yields could be bottoming. The daily RSI chart on the TLT is the most overbought it has been since early August of last year…just before the big decline in price (& the big jump in yields) began. We do have to admit that the TLT did become more overbought 2020 and 2019 before it rolled-over, so the TLT could indeed rise further before it tops-out. HOWEVER, those two instances took place during a “flight to safety” move in the Treasury market. In February/March 2000, it was the pandemic and the threat of a total economic shut-down…and in September of 2019 it was the freezing up of the repo market (the incident that most people have forgotten about).

Otherwise, the present reading on the RSI chart for the TLT is definitely at a level that has been followed by material reversals in the past. So, unless you see some sort of “flight to safety” move on the horizon, the RSI chart on the TLT is telling us that prices should top-out soon…and that long-term rates should bottom soon.

We’d also highlight the Bollinger chart on the 10yr yield. As a rather smart fellow highlighted to us late last week, it the yield on the 10yr note has fallen WELL below the bottom line of the Bollinger band, so it has become extremely oversold. So this is another reason to expect a bounce-back in long-term interest rates quite soon.

4) However, even if we’re wrong, inflation is not the only issue that would cause long-term rates to rise before too long. Therefore, we believe that the change in sentiment by many pundits about interest rates has changed far too quickly. We believe that those interest rates will begin to rise whether inflation is transient or not.

Last week’s data on inflation certainly did not indicate that inflation will be transient. Instead, it was merely the reaction in the bond market that led pundits to say that the Fed might just be correct in their assertion on this subject. In other words, there is no way to know if inflation will be transient or not.

Of course, the data did not indicate that inflation will gather steam in the future either. However, as we highlighted in the previous point, there are some technical reasons that can account for the strange move in the bond market recently. (Barron’s also highlighted a report from BofA that says insurance companies have been big buyers of bonds recently to fund annuities they write for corporations looking to do some creative accounting for their pension plans.) Therefore, there are several reasons to think the recent decline in rates is only technically driven and thus won’t last a lot longer.

That said, there are other voices around Wall Street that are saying that the growth in the second half of the year will be slower than the consensus is expecting. Some are highlighting the large drop in auto sales in May as a reason to think that second half growth is going to slow. Others are saying that recent decline in home-sales is a sign of an upcoming slowdown of growth in the second half of the year.

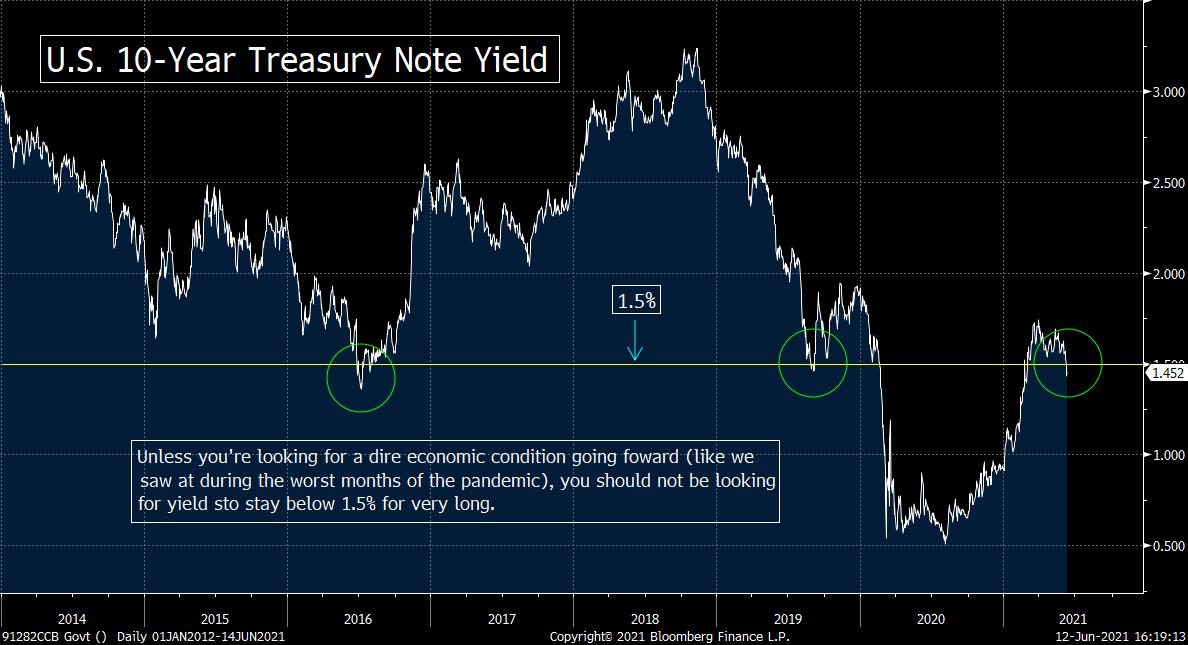

What do we think? Well, as we said above, we believe that the initial “pent-up” surge in the economy will indeed subside later this year. However, we do not believe it will fall back to levels that will justify long-term interest rates at a level below 2%. Let’s face it, except for a 2-week period in 2016 and for 4-days during the summer of 2019, the yield on the 10yr note has only fallen below 1.5% ONE other time in its HISTORY. Of course, we’re talking about the time-frame when the U.S. and the global economy almost completely shut-down. Do you really believe we’re in a situation right now is something that should keep interest rates at a level that is commensurate with the kind of economic back-drop we were facing when the economy was all but completely shut-down????

Sure, as we saw in 2016 and 2019, long-term interest rates CAN drop below 1.5% for a very short period of time. However, history also tells us that those kinds of moves into ultra-low levels do not last unless the economy is in a crisis condition. Therefore, we find it incredibly difficult to listen to the argument that says the growth prospects in the U.S. and around the globe will be at a level going forward that would justify long-term yields staying as low as they are today. In other words, the “natural level” for the U.S. 10yr yield is one that is much higher than it is trading at today in our humble opinion.

5) We used the term “natural level” in the last sentence of the previous bullet point because it is the term that Dallas Fed President Kaplan used recently when he said that he thought that he believed that long-term rates would drift higher. In other words, at some point in the coming months, the Fed is going to taper back on their bond purchases. Therefore, the supply/demand equation is likely going to shift enough to cause bond prices to fall and long-term yields to rise.

The one thing that people tend to forget when they are thinking about what is going on in the market place right now is that the Fed’s (and other global central banks’) massive stimulus programs were (by far) the number one reason why the markets were able to rally so strongly off of the March 2020 lows.

Actually, people DO understand this thought, BUT they cannot seem to let themselves believe that the CONTINUED rally (after the initial powerful bounce) has also been fueled mostly by the global central bank liquidity (along with some fiscal stimulus). They try to convince themselves that it’s the economic and earnings growth that if fueling the rally. In reality, however, earnings and the economy have merely been playing catch-up with the already elevated stock market. THIS IS WHY THE STOCK MARKET IS STILL EXTREMELY EXPENSIVE (at more than 22xx forward earnings and more than 3x sales) even though the economy and earnings have improved dramatically in the last year!

We hate so say it, but the comments we made in the last paragraph is a situation where we could say, “duh.” In other words, we think what has transpired over the past 15 months should be quite obvious to people. However, it is human nature for people to think their good fortune will continue because they convince themselves that the positive outcomes are based on natural events (and their smart choices) and not artificial manipulation by outside sources.

However, since the artificial stimulus IS still in full force, we believe it is the reason the S&P 500 is at its current levels…and not at 3,500…which would put it at a more reasonable 17x-18x earnings. (If interest rates rise, the range will actually still be considered expensive.) Once those forces become less helpful, the markets will react to that change.

Thankfully, the “artificial” stimulus will not be retracted all at one. However, many Fed officials (both present and former ones) have been laying the groundwork for the tapering back of their QE program. (Since we are no longer facing the struggles we were a year ago, this is the absolute right thing to do.) The Treasury Secretary has been laying the groundwork as well by saying that higher rates would be good for the country. (Why in world would she say this if she didn’t think/know that higher rates are on the way???)

Therefore, we are going to see a substantial change in the demand side of the supply/demand equation for the fixed income market. That means that interest rates will be meaningfully higher a year from now (and at the end of this year in our opinion.) This will happen whether inflation does or doesn’t accelerate in a pronounced fashion. It will merely be a more substantial rise if inflation becomes more than a transient development.

5a) We’d also like to add that the Fed , has ALREADY announced that they will taper very soon. By announcing that they will begin unwinding their corporate bond holding (their SMCCF program) IS an announcement of tapering! We don’t care that the certain present and former Fed officials try to claim that this is not a “taper” move.

No, we don’t want to call the Fed a bunch of liars, but they frequently try to sugar coat things so that their actions do not raise concerns in the marketplace. For instance, back in the fall of 2019, they said that the QE program that they began in order to deal with the freezing up of the repo market was not a QE program. BY DEFINITION, it WAS a QE program! However, the Fed did not want to cause any undue panic in the markets, so they tried to sugar coat it by saying it was not a QE program…….They are doing the same thing today when they try to say that the unwinding of the corporate bonds on their balance sheet is not “tapering”.

BTW, when the Fed engaged in their 2019 “not QE program” in late September/early October of that year, the stock market rallied more than 15% in just four months…even though the market was expensive based on stated earnings before the further rally began. (Go figure.) The Fed engaged in a new stimulus program…and the stock market rallied. Therefore, as the Fed begins engaging in “tapering” (like they have just announced they will do with the SMCCF program), we should expect the stock market to give back some of its gains.

6) The European stock market has outperformed in recent months. As they ease-off on their pandemic restrictions, the European economy and stock markets could/should outperform the U.S. in the coming months as well. However, this market is also becoming quite overbought on its weekly RSI chart, so investors and traders should be a big careful over the near-term.

The U.S. stock market has outperformed the European stock market by a wide margin so far this year. However, since the end of April, the STOXX Europe 600 Index has begun to play catch-up a little bit. It has rallied 4.6% while the S&P has rallied just 1.5%. Given that the Europeans have taken longer to lift their pandemic restrictions, the recent outperformance could/should continue as those restrictions are indeed lifted.

Having said this, however, we do need to point out that the European stock market is becoming overbought. In fact, it has now reached a level that has been followed by pull-backs pretty much every time over the past five years or so. Its weekly RSI chart has moved above 74. That might not sound like an extreme level, but for the STOXX Europe 600 Index that is on par with the most overbought readings we’ve seen since the financial crisis. Therefore, it raises a yellow flag on European stocks on a near-term basis.

The good news is that some of the pull-backs that have followed its present RSI level were not major ones at all, so any upcoming weakness might merely be something in the 5%-7% range. That would not be a big concern for long-term investors at all. However, since SOME of those declines have been full blown corrections, investors and traders alike should be a bit careful about chasing European stocks over the near-term.

7) For the third time in five months, the SMH semiconductor ETF has traded up within the 250-260 range. Each of the other two times it has fallen back. One of the key reasons for this is because the stock with the highest weighting in the SMH (by far) has been acting quite poorly. We’re talking about Taiwan Semiconductor (TSM) and thus how it acts over the coming days and weeks should be important for the group (and the market overall).

One group which could determine which way things will go in the stock market over the summer months is the semiconductors. The chip stocks have acted well in recent weeks, but this has only taken the SMH semiconductor ETF back up to a level that it has reached two other times. Therefore, it has been unable to make much progress after hitting an all-time high back in February.

The main reason it has been unable to breakout is the poor performance in two names: TSM and Micron (MU). Even though the broad semiconductor space has acted well in recent weeks, TSM and MU have not joined in on the fun to the same degree that others have (like NVDA). Yes, they have both bounced, but TSM still remains a full 15% below its April highs and MU is 17% below its own highs. TSM has become the most important semiconductor company in the world, so the fact that it is lagging badly has got to be weighing on investors minds when it comes to the entire group. (BTW, when looking at the chip sector, we like to use the SMH semiconductor ETF, rather than the SOXX, because it is much more liquid.)

Since we wrote about this issue on Wednesday and spoke about it in an interview with CNBC.com (which is attached below), this subject has also popped up in Barron’s. This week’s edition of Barron’s has an article on TSM that basically says investor should wait for the stock to drop further before buying the name. They quote several analysts who say that TSM is a great company, but that is has become quite expensive (27x next year’s earnings vs a 5yr average of 19x). They also sight lackluster demand for smartphones and the geopolitical tensions between China and the U.S. as headwinds for the stock going forward. One analyst said it “needs to shed another 15% to adequately reflect the current risk profile.

If TSM falls another 15% (down to $100), that will take it well below its “double-bottom” lows of $109 from March and May. That kind of development would be very bearish for the rest of the SMH…given that TSM is almost 15% of the SMH. With stocks like MU (and AMD as well) struggling in recent weeks/months, that leaves a lot of work for other stocks to do to make up the difference. (That might be tough to accomplish given that NVDA is becoming overbought on a short-term basis.)

Of course, maybe TSM can gather itself and regain some upside momentum. It if can indeed do so…and it can move back above its early April highs of $125, it will give the stock some badly needed relief. If, however, it rolls-back over and takes out that “double-bottom” low of $109, it’s going to be quite bearish.

Therefore, the battle lines are well drawn for TSM. Whichever line it breaks first (in a meaningful way) should be an important indicator for which way this stock is going to go over the summer. Since TSM is such an important stock for the chip sector, its move will be important for the SMH as well. Finally, given that the semis have been such an important leadership group over the years, the next big move in TSM could be important for the entire stock market.

Semiconductor stocks lag tech in comeback. Two traders on what's next (cnbc.com)

8) We have been very bullish on the energy sector for most of the past 8-9 months. We are still quite bullish, but we do need to point out that natural gas is getting overbought on a technical basis. Therefore, it looks like it is getting ready for a pull-back. If that indeed takes place, it could/should cause some of the energy stocks with a large exposure to nat gas to pull-back as well.

Natural gas has rallied almost 35% since early April, so there is no question it has seen a nice run. The rally has taken the commodity up near highs from November of last year. If it can move above that level, it will give it a very nice “higher-high”…which would be quite bullish on a technical basis. However, nat gas is becoming overbought on a near-term basis. No, it is not an extreme reading. The 73 number on its RSI chart has been exceeded several times over the past few years. However, whenever any asset reaches a key resistance level at the same time it is becoming overbought, experience tells us that it usually takes a “breather” before it takes a more realistic run at breaking its key resistance level in the kind of meaningful way that will make it a compelling (and long-lasting) breakout.

In other words, if natural gas can see a mild pull-back (a “breather”) that helps it work-off some of that overbought condition, it will give it a much better chance of avoiding a “head fake.” It will give it a better chance of turning the “breakout move” into a powerful one over the coming weeks and months…and not something that “fails” within a few days or a week.

We’d also note that some of the individual energy names whose stocks are more sensitive to moves in natural gas are getting overbought as well. For instance, the weekly RSI chart on Kinder Morgan (KMI) has moved up to the 72 level (71.92 to be exact). That’s not very extreme when you compare it to the readings we’ve seen in stocks like VIAC, GME, and AMC in recent months, BUT it is still the highest reading we’ve seen in KMI since 2012! Therefore, it’s something that is getting our attention.

Both natural gas and KMI (& other nat gas stocks) could still see more upside follow-through over the coming days, but we think the commodity and those individual stocks are getting ripe for at least a “breather” soon and thus they should not be chased in an aggressive manner right now.

9) The corrections in Bitcoin and other cryptocurrencies this year have not had a material impact on the broad stock market. However, as the Fed moves closer to tapering back on their bond purchases, the moves in this asset class could tell us something about the impact a less accommodative Fed my have for other asset classes as well. Therefore, we thought we’d look at the chart on Bitcoin once again this weekend.

We’ve seen three deep declines in Bitcoin and the other cryptocurrencies this year. Back in January, Bitcoin dropped almost 25. In March, it declined by about 20%. Of course, as we all know, it has fallen by more than 45% over the past two months. However, none of these moves has had a negative impact on the stock market at all. The last time we had a pull-back in the S&P of more than 5% was when God was a child!

Bitcoin and the other cryptos has seen extended declines in the past. They have also “stayed down” for a while in past years as well. However, from the March 2020 lows until the spring highs, ALL of the sharp declines we’ve seen have been followed by sharp bounces almost immediately…until now. The most recent decline that bottomed in late May has NOT seen a sharp bounce. Instead, Bitcoin has been trading in a range over the past three weeks.

On a closing basis, that range has been between $33,700 and $39,000. On an intraday basis, it has been a much wider range (between $30,000 and $40,000). Usually, we put a lot more emphasis on closing prices when we look at the charts, but due to the fact that Bitcoin is such big asset with individual investors, we think the “round numbers” involved with the intraday range will be the more important ones this time around. (Individual investors just love round numbers…and are much more likely to react to a break of those round numbers…in either direction.)

None of what we just said means that Bitcoin is going to breakout of this 3-week range soon. If the stock market can remain range-bound for many months, the cryptocurrencies can certainly do the same thing. Therefore, we’re NOT saying that we’re about to see an imminent move outside of its range. We’re just saying that IF it DOES breakout of the $30k-$40k range in the next week or two, it should be a VERY important development for Bitcoin and the other cryptos.

However, we’re ALSO saying that is could have an impact on other assets as well this time. As we’ve said in our previous bullet points, the Fed has told us that they’re already going to unwind their corporate bond portfolio. Thus, they’ve actually already begun to “taper.” If they start talking about tapering back on their other bond purchases in the days and weeks ahead, it could/should have an impact on the amount of excess liquidity that is sloshing around in the system.

Therefore, if Bitcoin can breakout of its range to the upside, it might just be telling us that there’s still plenty of liquidity in the system to keep many assets rising. If, however, it breaks its range to the downside, it might be telling us the exact opposite is taking place.

10) Summary of our current stance……The S&P 500 Index has made multiple new all-time highs this year, but the ones that it has made more recently have been very slight ones. Yes, it does SEEM like the market has continued in a sharp upward trajectory. However, that’s due to the fact that several different asset classes have taken turns experiencing parabolic rallies. However, the S&P is only marginally higher than it was two months ago, and both the Nasdaq and Russell 2000 are actually slightly below where they stood 4-5 months ago. Therefore, there is no question that the rally off the March 2020 lows has stalled out. This does not mean it cannot see another rally leg now or in the near future, but we believe it’s important to keep things in perspective. The rally in stocks is not as strong as it once was.

We also believe that the decline in interest rates that we’ve seen since March has more to do with technical factors than fundamental ones. Thus, we think it is quite likely that they will resume their rise soon (especially since Treasury prices have become overbought on a near-term basis, and yields have become oversold.)

More importantly, we believe that Dallas Fed President Kaplan is correct and that those rates will drift higher and reach a more “natural” level. This should take place EVEN if inflation does not rise in a powerful way and EVEN if the rate of growth in the U.S. slows some-what in the second half. In other words, the demand side of the supply/demand equation has had a HUGE impact on the level of interest rates over the 15 months. Now that the demand side is going to start do diminish as the Fed tapers back on its QE program (and already announced that it will begin doing so very soon with their corporate bond holdings), the move in long-term interest rates should be to the upside.

Of course, we could be wrong. However, if we are wrong, we think it will be on the timing side o

Recent free content from Matt Maley

-

THE WEEKLY TOP 10

— 10/23/22

THE WEEKLY TOP 10

— 10/23/22

-

Morning Comment: Can the Treasury market actually give the stock market some relief soon?

— 10/21/22

-

What Do 2022 and 1987 Have in Common?

— 10/19/22

-

Morning Comment: Which is it? Is stimulus bullish or bearish for the stock market?

— 10/17/22

-

Morning Comment: Peak Inflation is Becoming a Process Instead of a Turning Point

— 10/13/22

-

{[comment.author.username]} {[comment.author.username]} — Marketfy Staff — Maven — Member

- 1 Campus Martius, Suite #200Detroit, MI 48226

- +1 877 440 9464