THE WEEKLY TOP 10

If you would like to get these unique insights on a regular basis during these fascinating times in the investment world, please click here to subscribe to “The Maley Report.”......Thank you very much.

THE WEEKLY TOP 10

Table of Contents:

1) The Fed to let inflation run hot...which = higher LT interest rates...which = lower stock prices. (Pretty simple.)

1a) Following last year’s script..........And...the Fed knows higher inflation will hurt the broad stock market.

2) Having said this, the Fed’s goal is still to keep these moves gradual ones.

3) More examples of “forced selling”...that’s what happens in an extremely leveraged marketplace.

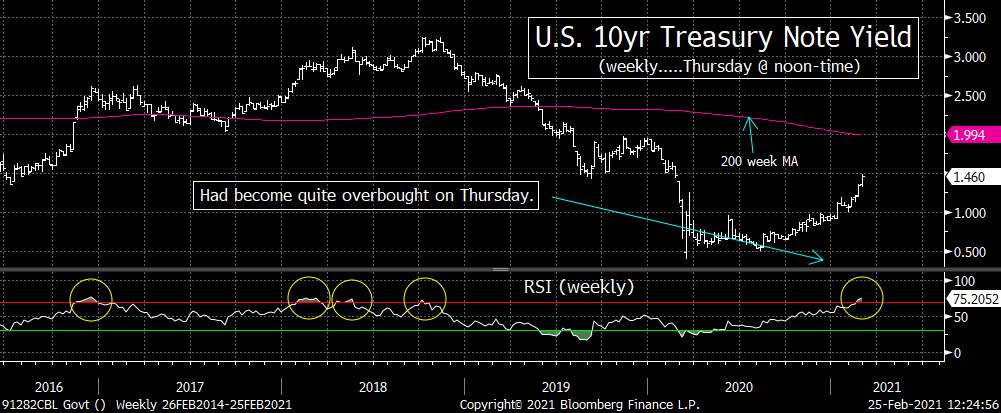

4) Treasury notes have become very oversold near-term. (Overbought in terms of yield.)

5) Support/resistance levels for the S&P 500, Nasdaq, and Russell 2000 indices.

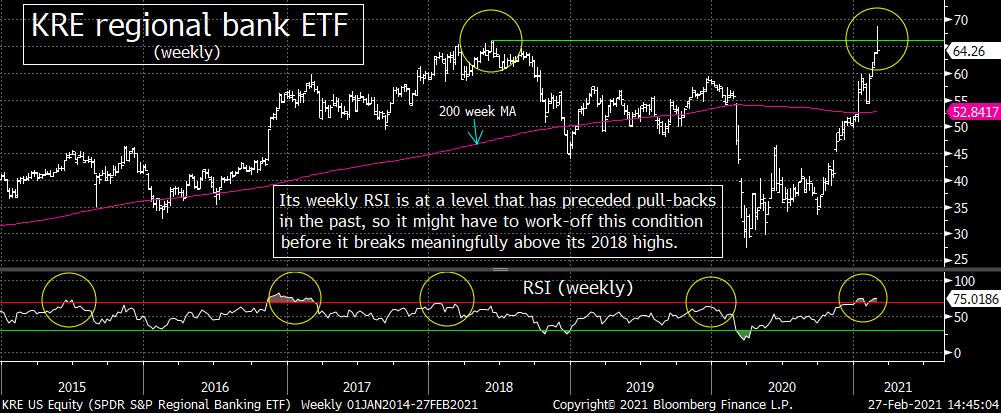

6) With T-notes oversold, bank stock have become overbought...and due for a “breather.”

7) We’re seeing signs that the “tradable” pull-back in commodities is beginning.

8) The travel & leisure stocks have become very overbought. (New Covid Variants to cause problems?)

9) Quick comments & charts on Bitcoin, TSLA, Gold, and the ITB housing ETF.

10) Summary of our current stance.

Long (and only) Version:

1) Chairman Powell’s comments last week were dovish...and thus they were originally viewed as bullish for the stock market. However, the more important aspect of his comments was that he reiterated the Fed’s intention to let inflation run hot. That’s good for the economy, but it also means that the Fed will accept higher long-term interest rates...so it’s not so great for the stock market for the near/intermediate-term.

Chairman Powell’s comments in front of Congress last week were bullish for the economy, BUT they were not particularly bullish for the stock market. Even tough they’re willing to keep their stimulus programs in place for as long as is needed to make sure that the recovery will continue, he also reiterated that they are willing to let inflation run hot. That’s great for growth, but higher inflation means higher long-term interest rates...and that’s not good for a stock market that stands at extreme levels of valuation.

(Traditionally, the Fed does not control long-term rates...only short-term rates. However, with their massive QE program, they can impact longer-term rates more than they have in the past. Since Mr. Powell is telling us that the Fed is okay with a higher rate of inflation, it means that he’s okay with longer term interest rates moving higher than most people thought was possible just a short time ago.)

Of course, these higher long-term interest rates have an impact on what investors are willing to accept in terms of valuation. This is particularly important for the tech stocks...whose cash flows are a long-term play....and thus higher rates will create a situation where investors will not accept the kind of sky-high valuations that they’ve been willing to accept in recent years. However, this is not only true for the tech stocks. The entire stock market was very expensive, so if rates continue to rise, it’s going to create a big head-wind for the stock market as we move through 2021.

In other words, the Fed pushed asset prices well above their economic value with the massive liquidity program last year...so now it’s time for them to help economy play catch-up to the stock market.......The problem is that with interest rates rising in a very expensive market, the economy & the market will likely meet at some point in the middle...which leaves the stock market vulnerable to a correction.

1a) That said, this does not necessarily mean that the stock market will fall out of bed next week. (IF it does fall out of bed, it WILL be the kind of Twilight Zone moment we described last weekend...because it will show that we’re continuing to follow what took place at the beginning of last year in the same EXACT way!) Anyway, just because the Fed is telling us that they’re okay with higher inflation...and thus telling us they’re okay with higher long-term rates and lower asset prices, it does not mean that they’d like to see these moves happen all at once!

Even if we’re correct (and the Fed is really telling us that since their okay with inflation running hot for a while...and therefore they’re also okay with higher LT interest rates...and thus okay with lower stock prices)...it does not mean that they want these moves to take place immediately. In fact, if they learned anything from the “taper tantrum” of May/June 2013, it’s that it works much better if the process plays-out over an extended period of time. As we have said in previous notes, the Fed’s goal is for the markets to price-in most of the tapering-back of their QE program before they actually end the program. (That’s what they were eventually able to do later in the summer of 2013 and early in the fall of that year.) However, the Fed knows that if it takes place too quickly, it will create a lot problems....so they would love to see this process playout over time.

Of course, the Fed could lose control of the situation......However, what we’re trying to say is that the fact that long-term rates are rising does NOT mean that the Fed has lost control (at least not yet). In our opinion, they KNEW rates were going to rise...and they KNOW that they’ll continue to rise over time...and they’re okay with this development. Since the know that higher rates are not stock market-friendly, it means that they’re okay with a decline in stocks. In fact, it’s not out of the question to think that they’d actually LIKE the stock market to see a correction (as long as it doesn’t get out of control)...because it will take some of the froth that has popped up in the marketplace over the past few months.....In other words, just because the Fed does not want to lose control of the situation does not mean that they want to keep the stock market elevated (like they have in the past).

2) Even though we think that the Fed will accept a rise in long-term interest rates, they still have their massive QE program at their disposal. Therefore, we do not believe the rise in long-term rates will continue at the same speed we saw last week. In other words, the Fed’s goal is to let inflation rise and thus let long-term rates rise GRADUALLY. That’s STILL not good for stocks, but it should help us avoid a major bear market.

We thought that the comment former NY Fed President Bill Dudley made this week in one of his regular musings for the Bloomberg print outlet was very accurate (and very telling). In the piece, he said that he continues to see inflation moving higher in the future, BUT he also said that he does believe it to turn into run-away inflation.....However, he also said that as the process of inflation moving higher will “ultimately...leave U.S. interest rates higher than they’ve been in a long time.” He went on to say, “The bad news is that the transition will likely be painful for financial markets. The good news is that the Fed will have more firepower to fight the next recession.”

So when you combine these comments with the words of Chairman Powell from this past week, A LOT of people associated with the Federal Reserve (both past and present) are concentrating on inflation. Both Powell & Dudley told us last week that we should not worry about U.S. inflation. It very likely coming, they say...as several forces are converging to push price higher. The big fiscal stimulus packages that are coming from Washington DC in the future and the release of pent-up demand when as the economy re-opens...means inflation is headed higher. However, they do not seem worried that it will become a major problem because the economy is a long way from operating at capacity...and that inflation is a slow-moving process. Also, another reason Mr. Dudley sighted was that “all the central bank has to do is tighten monetary policy by raising short-term interest rates” if the situation starts to run too hot.

However, the thing that really stood out to us from last week’s “Fed comments” is that they went out of their way to tell us that a rise in inflation will not be a big problem for the economy. They’re telling us that the economy will be fine...and that it could/should grow nicely...even though inflation is going to rise (because inflation is not going to get out of control). HOWEVER, they did NOT say that the markets will be fine. In fact, Mr. Dudley’s comments indicated that he is expecting higher inflation to have the exact impact on the stock market.

In other words, given that Fed Chairman Powell is telling us that inflation is going to increase...and thus long-term interest rates will increase....he’s really telling us (in an indirect fashion) the overt consequence of these moves is that a new headwind for the stock market and other risk assets is now upon us...........However, the former NY Fed President was MUCH MORE direct. He flat-out SAID that this process will be negative for financial assets!

When the former NY Fed President says that interest rates are likely going to move “higher than they’ve been in a long time”....and that it is “likely to be painful for financial markets”...it tells us that the goal for the U.S. Federal Reserve has changed since Ben Bernanke was the Chairman in our opinion.Coming out of the financial crisis, it was the Fed’s (publicly) stated goal to push asset prices higher...in the hopes that it would help spur growth. However, that was when asset prices were very cheap......Now that asset prices have become very expensive (and some are seen to be at bubble levels)...the Fed seems be much less focused on using asset prices as a tool to help the economy today.

To be very honest, we strongly believe that the Fed is doing the right thing. Their policies since the financial crisis have helped push asset prices decidedly above their fundamental values. That can only last so long. Eventually, the stock market needs to trade at a level that is in-line with its underlying fundamentals. Today, that just might mean that the stock market needs to slide lower....while the economy improves...and they meet somewhere in the middle. (It’s hard for the economy to catch-up to a sideways stock market...and especially to catch up to a rising stock market...when the economy & the stock market get divorced from one another in a major way. The stock market usually has to pull-back some-what...even if the economy is improving...when the stock market pulls too far ahead of the economy....like it has in recent months.)

3) We are worried about two themes that we read and heard about several times in the last week or so. The first one dealt with an opinion that said we don’t have to worry about Thursday’s big decline in the bond market (& the rise in rates that went with it) because it was an artificial move and had little to do with fundamentals. The second topic was one that we heard about the chances that we’ll see a 10% correction in the stock market. Due to the issue of leverage, these are not benign issues at all!

Late last week, we heard and read discussions about how the outsized drop in Treasury prices on Thursday (and thus the outsized rise in long-term interest rates) was something we don’t have to worry about...because it was an artificial move and did not have a lot to do with fundamentals. That’s ridiculous.

First of all, at least SOME of the rise in rates had to been due with the recent improvement in the economic data AND the comments about inflation from Chairman Powell last week (and other Fed members recently). Second of all (and most importantly), the artificial (“forced”) selling of bonds on Thursday should be a MAJOR concern for investors!!!!

The story that we heard about dealt with a crowded positions in the Treasury futures market that was “forced” to be unwound after the poor Treasury auction on Thursday. We do agree that this may have exacerbated the rise in rates. However the much more important issue with this development is that it’s another example of what can happen in a HIGHLY leveraged market (like the one we have today). First it was the squeeze of the highly leveraged short positions in stocks like GME, AMC, KOSS, etc. Then the same thing happened to the cannabis stocks. NOW we see the problem showing up in the bond market!

The fact that we’re seeing more and more crowded trades being “forced” to unwind themselves....and this shows the dangers of a market that is HIGHLY leveraged. History is filled with examples of when a few small bouts of “forced selling” are merely the warning signals of a much bigger wave of “forced selling” that comes at a later date...and involves several different markets. (Remember, the 2008 crisis began with a round of “forced selling” in two credit hedge funds run by Bear Stearns in the summer of 2007...about two months before the top in the stock market. Six months later, Bear Stearns went belly up...and 14 month later, Lehman collapsed.).....No we’re not calling for 2007-2009 style collapse, but these first few small waves of “forced selling” could easily be a warning of something bigger to come...and investors are not paying enough attention to this possibility.

The second issue deals with the growing calls from pundits who say we’re in store for a 10% correction. We have been saying that any upcoming correction will be a deeper one (in the 15%-20%) range. Very simply, in a highly leveraged market, it’s almost impossible to keep a decline in the 10% range. Sure, if it’s only 5%-7%, that’s fine. However, when a highly leveraged stock market falls 10%, THAT’S when the margin calls start to kick-in. Therefore, it is more likely in our opinion that the issue of “forced selling” will all but insure that a 10% correction will turn into something bigger.

This does not mean that we’ll see the same kind of wave of “forced selling” that knocked the S&P 500 down 35% last year. We believe that the Fed will step to the plate before things get that bad. However, it will still be difficult for them to keep the market from falling “just” 10% when it is as highly leveraged as it is right now.

If we do see a deeper (15%-20%) correction, it will certainly be very scary for investors. However, those who are prepared for such a move will get a fabulous buying opportunity at some point in the future.......Don’t fear corrections...embrace them!!

4) Having made several bearish comments about the Treasury market, we HAVE to highlight that it is becoming very oversold on a short-term basis. (Very overbought for long-term yields.) Therefore, the Treasury market is getting ready for a short-term bounce in price (and thus a near-term drop in rates)...and we saw some of that move already on Friday. The strange thing is that any bounce in bond prices (drop in yields) could get exacerbated if the stock market sees a meaningful decline from its extended/expensive level due to reasons other than rising yields. (In other words, if the stock market falls for a reason that has nothing to do with interest rates (like a big upswing in Covid cases due to the new variants)...the stock market will likely fall even as yields fall at the same time. Thus there is no guarantee that a drop in rates will CAUSE a rally in stocks. It could turn out that a decline in stocks CAUSES the rally in bonds (drop in yields) from its oversold level.

Needless to say, you can guess from what we’ve been saying so far that we still believe that long-term yields will continue to head higher over time. However, since the TLT Treasury ETF (which measures bond prices, not yield) had become quite oversold on Thursday, we think it will likely see a near-term bounce...one that will last for more than just 1 day. (This, in turn, would obviously mean that bond yields will likely see a near-term pull-back.)

However, this does not mean that it will be a “tradeable” bounce in prices (fall in yields) that lasts for several weeks. It just means that investors and traders should hold-off in being aggressive on the kinds of assets that will benefit from higher interest rates for a little while. (They should also hold-off in being aggressive in making negative bets on assets that will be hurt by higher interest rates.)

Looking at the RSI chart on the TLT, it fell to the 18 level on Thursday...which is the most oversold it has been since 2016. So it’s not a stretch to think that this bounce in price will last for a few days...maybe as much as a week or so. We do admit that last time the TLT got as oversold as it did on Thursday, it was followed by a bounce in prices (pull-back in rates) that lasted a full month. We suppose that this could happen again this time, but given that the yield on the 10yr T-note has confirmed a change in trend recently (by breaking WELL above its trend-line from 2018 and WELL above its early 2020 highs), we’re thinking that short-term reversal will not last as long. (The pull-back in LT rates in late 2016 took place within an down-trend that was still fully in tact.)

We called for an important change in trend for long-term interest rates back in late August...and that call has worked out EXTREMELY well. Shortly after we made that call (in September), we also turned bullish on the bank stocks (after almost 3 years with a cautious stance on the group). That call also worked out very well...as the KBE rallied over 80% and the KRE basically doubled!.

Since we’re only calling for a near-term pull-back in long-term rates, we’re not saying that investors should take profits in the group. Instead, we’re just saying that they should be much less aggressive over the near-term. Traders on the other hand, might want to take a few chips off the table. This worked out very well when we made the same call in mid-January, but its still a group where traders should keep some long positions. We just think there will be better levels where we can add to these names over the next week or two..........Longer-term, this group should continue to be a great one in 2021. (We go into more detail on the KBE and KRE charts in point #6)

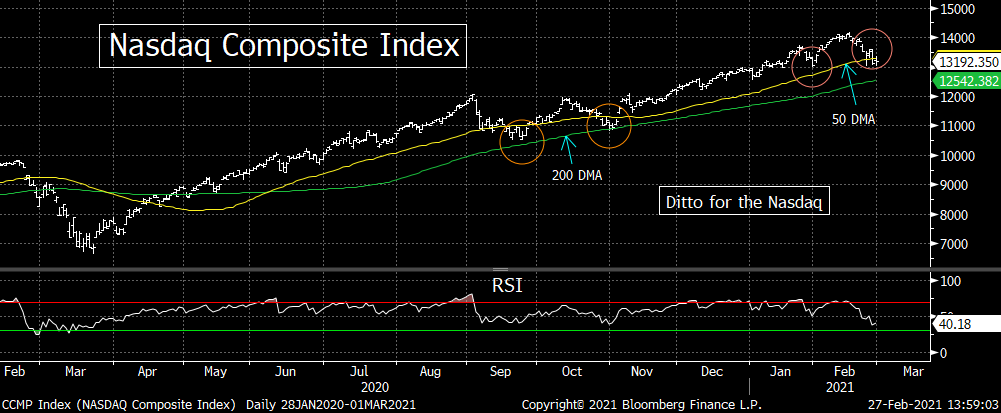

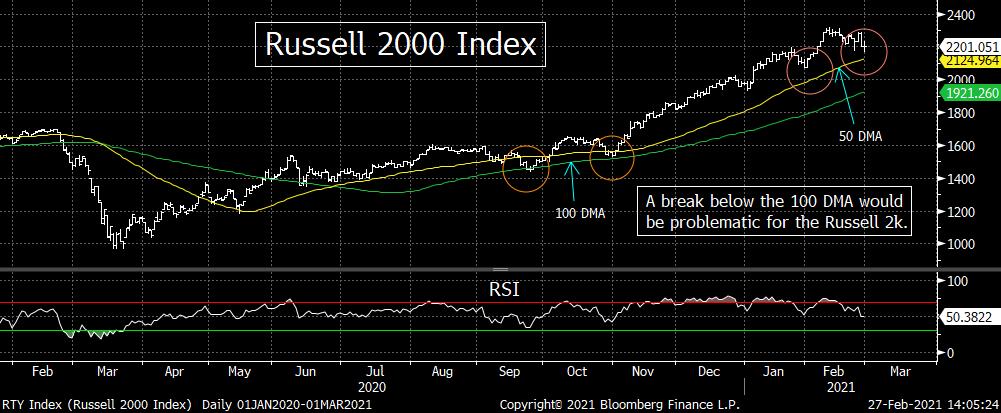

5) With a new wave of volatility hitting several different markets this past week, we thought it would be a good idea to highlight the key support and resistance levels on the S&P 500, the Nasdaq Composite, and the Russell 2000 indexes. The key resistance level for all three is obviously the recent record highs. As for the first two support levels, it’s the 50 DMA and the 100 DMA for all three indices (and especially true for the SPX). If things get ugly, the more important support levels come-in about 15% below the recent highs for the S&P & the Nasdaq...but more than 20% below the February highs on the Russell.

If the stock market sees more weakness as we move into the month of March, the first two support levels we’ll be watching on the S&P 500, Nasdaq Composite, and Russell 2000 indices are well defined...and very easy to keep an eye on. For all three indices, the first support level is the 50 DMA...and the second one is the 100 DMA. It’s usually not that easy, but it IS just that easy this time around.

The 50 DMA for the S&P, indices is the line that held when the GameStop debacle was hitting the market late in January...and it held that line on Monday as well...when TSLA and Bitcoin got hit so hard. (Actually, the Nasdaq fell slightly below that line on Monday and closed slightly below it yesterday....and the Russell was able to bounce from just above its 50 DMA on those two occasions. However, both were close enough to the 50 DMA to make it the first level to watch for support on these two averages.)

That said, the 100 DMA is going to be more important. That was the line the stopped the declines we saw in both September and October of last year for all of them. Therefore, a meaningful break below that moving average would raise our concerns to a much greater degree.

Don’t get us wrong, we’re not saying that the 100 DMA is some sort of major “line in the sand” for these averages. It’s just the second support level of the first two levels we’ll be watching over the near-term...if (repeat, IF) the market does indeed see some more downside follow-through in March.

The much more important support level will be at the 3275 level on the S&P 500. That would give the SPX a Fibonacci 38.2% retracement of the total rally from last March...AND it was the lows we saw in September andOctober. So that level will be a MUCH more important level. However, that’s 16% below the recent all-time highs, so we’re not going to worry about that one just yet.

For the Nasdaq, the more important level is the 10,500 level. That was the lows from the 12% correction this index experienced in September...and would give us a 50% retracement of the rally from last March. (The rally in the Nasdaq since last March has been stronger than it has been in the SPX, so it makes sense that it would see a deeper retracement if...repeat, IF...things get ugly.)........Finally, the 1800 level is the one we’ll be watching for the Russell 2000. That’s where the trend-line from the March lows comes-in...and it’s also a Fibonacci 38.2% retracement of the rally from the lows last March.

Any break below these more important support levels on all of these indices will mean that there is something more serious going on...and that a bear market is quite likely........We’re a long way from those “line in the sand” levels, so we’ll be concentrating on the 50 and 100 DMAs on these indices for now.

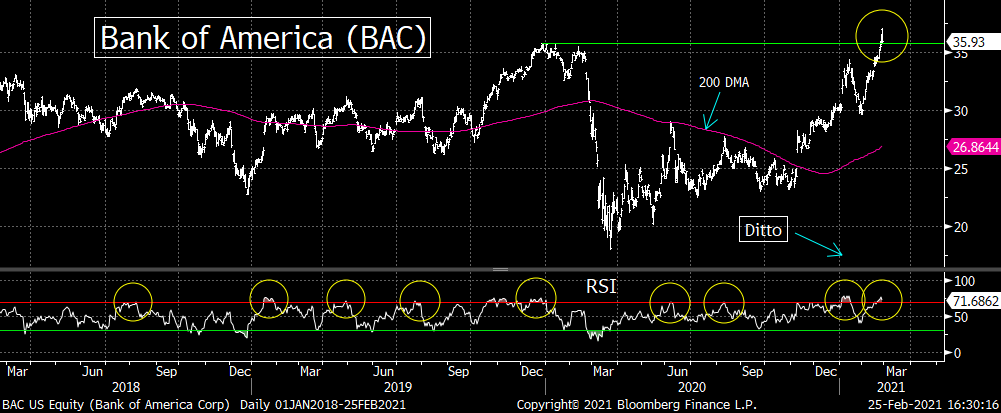

6) Ok, lets look at the charts on the groups that had become very overbought by mid-week last week. Some of them were interest rate related, but others became overbought on their own. Let’s start with a couple of the interest rate sensitive groups...the banks and the techs. We’ll start with the bank stocks. Both the KBE and KRE bank ETFs (along with several key individual bank stocks) had become quite overbought mid-week last week.

As we highlighted in point #4, the Treasury market has become extremely oversold on a short-term basis (overbought for yields). Thus it should be no surprise that when you look at the KBE & KRE (and the broader XLF financial stock ETF), they had also become quite overbought by Wednesday’s close (after Chairman Powell made his dovish comments in front of Congress...for the second day in a row). In fact, as you can see from the attached charts, the weekly RSI for these two ETF charts had reached levels that had signaled tops over the past 4-5 years (at least on a near-term basis). Therefore, they were getting ripe for the kind of pull-back that will last more than just 1 or 2 days. (This something we also highlighted in a CNBC interview on Thursday afternoon. Click on the link below to see the interview.)

Both of the bank ETFs were testing their 2018 highs, so it was a key technical juncture for these stocks, but we think they are too extended on a technical basis to make material “higher-highs” over the near-term. We DO think they’ll break above those highs in a meaningful way eventually, but we’re thinking they’ll have to digest their recent gains before they break above those 2018 highs in a significant way.

We don’t see a major correction in these bank names, so long-term investors can continue to nibble on them...but I think they should hold-off in being aggressive again until after these technical conditions are worked-off. (Short-term traders should take some profits on any further advance...and look to reload on the group at lower levels.).....We also think the same strategy should be followed for other groups that will be effected by rising yields.

We turned bullish on the bank stocks back in September (long before the consensus jumped on the band wagon). So after a rally of more than 80% in just five months, we can afford to miss a little bit of upside movement if we’re wrong about a correction at these levels. However, given how overbought these ETFs have become (and how oversold the Treasury market has become), we don’t think the sector will run away from us at current levels.

(We have also provided the charts on two specific big-cap bank names...JPM & BAC...that we drew-up on Thursday. These two names have made significant “higher-highs,” so they look great longer-term. However, they’re also very overbought, so they’re ripe for a pull-back as well.

6a) We want to update our comments from last week about the technical levels of the FAANG stocks. None of them broke below they key support levels we highlighted last weekend....but three of them certainly got close. GOOGL still acts fine. It fell pretty hard early in the week, but it didn’t see much downside follow-through later in the week. Also, NFLX was basically flat on the week...so it’s holding-up okay. However, FB, AAPL, AMZN all closed right on the key support levels we highlighted last weekend. Therefore, any downside follow-through next week will be negative for these three stocks on a technical basis. (See last weekend’s piece for the charts.)

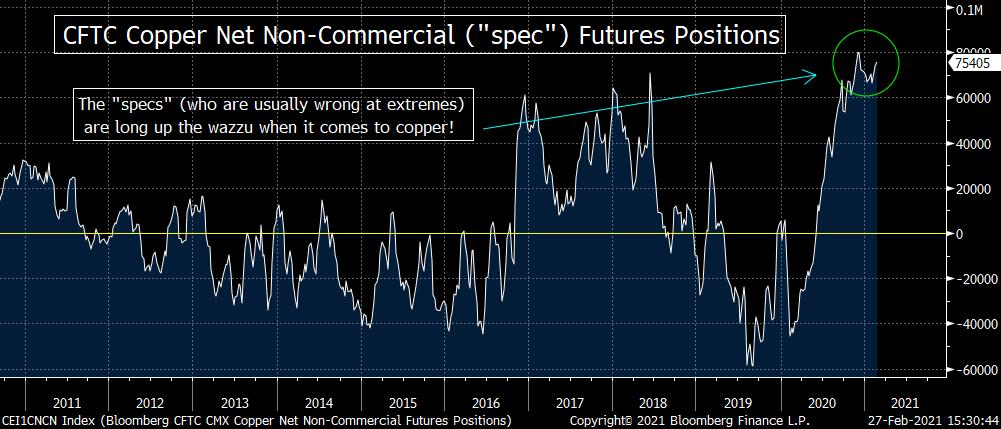

7) We were a little early on our cautious near-term call on commodities, but since we were not very early at all...and since we have turned bullish on this asset class early last summer...our batting average on commodities remains an excellent one. We are now seeing the beginnings of what we think will be a material pull-back. The decline in the CRB, copper, gold, etc. that we saw late last week was not enough to confirm anything yet. However, given how overbought the asset class has become...and given the renewed strength of the dollar, we think that we’re in the early innings of a “tradable” decline (one that will likely last longer than the pull-back in LT interest rates we described above).

We finally saw some signs that commodity space is going to see a pull-back...as the CRB commodity index fell pretty hard on Friday and specific commodities like copper, gold and lumber all got hit hard as well. As we highlighted last weekend, these commodities had become EXTREMELY overbought on their daily and weekly RSI charts by last weekend, so they were ripe for a material pull-back. (They became even more overbought by mid-week last week....as the daily RSI for copper moved above 87 and it moved above 88 for the CRB at one point!)

If this was the only reason why we were concerned about this asset class, we’d merely be calling for a very-short-term decline. However, since we think that the dollar will likely see a strong “tradable” rally over the coming weeks, we think that the decline in commodity asset class (and the commodity related equities) will last longer than it will for the interest rates sensitive groups (like the banks).....We’d also note that the “positioning” in commodities like copper (where the COT data shows that the net long positions for the “specs” are huge) is another reason to think that the decline in copper & other commodities will last for a while.

Going back to the dollar, we just believe that the “short dollar” trade is much too crowded to induce the dollar to fall from current levels. The downside trajectory of the DXY dollar index had already stabilized in January...and its strong bounce on Friday is something that could be telling us that a more meaningful bounce in the greenback is dead ahead of us. Since the COT data shows that the dumb money non-commercial traders (the “speculators” or “specs”...who are usually wrong at extremes) have HUGE net short positions, we believe there is nobody left to sell (or short) the dollar. When you combine this with the bearish sentiment in the dollar that has existed since last year...and you have a good recipe for a “tradable” rally in the U.S. currency. Given the strong inverse correlation between the dollar and commodities, we want to steer clear of the commodity asset class for the time being.

We want to reiterate that we still believe that we are in the early innings of a long-term bull market (after a multi-year bear market since 2011). However, no long-term bull market moves in a straight line, so we want to be much less aggressive on the long side of this asset class over the coming weeks. If we get some downside follow-through soon early next week, we think short-term traders should consider making bearish bets on the sector...but with the knowledge that this will not be a long-term play.

8) We’re afraid that the travel & leisure names became VERY overbought mid-week last week as well. For instance, stocks like Southwest Air (LUV), Royal Caribbean (RCL) and Marriot (MAR) had become the most overbought they’ve been for many years. This tells us that they’re getting ripe for a short-term pull-back...AND it could become a deep decline if a new wave of the coronavirus hits us. (More experts are sending up some warning signals.)

There is no question that many of the travel & leisure stock had become quite overbought mid-week last week. On top of the fact that stocks like Southwest Air (LUV), Royal Caribbean (RCL) and Marriot (MAR) have become the most overbought they’ve been for many years... both the daily and weekly RSI charts for the XAL airline ETF have reached

Recent free content from Matt Maley

-

THE WEEKLY TOP 10

— 10/23/22

THE WEEKLY TOP 10

— 10/23/22

-

Morning Comment: Can the Treasury market actually give the stock market some relief soon?

— 10/21/22

-

What Do 2022 and 1987 Have in Common?

— 10/19/22

-

Morning Comment: Which is it? Is stimulus bullish or bearish for the stock market?

— 10/17/22

-

Morning Comment: Peak Inflation is Becoming a Process Instead of a Turning Point

— 10/13/22

-

{[comment.author.username]} {[comment.author.username]} — Marketfy Staff — Maven — Member

- 1 Campus Martius, Suite #200Detroit, MI 48226

- +1 877 440 9464