The NEW Daily Decision for 11.2.18 - Of Jobs, Apple, and Trade

Portfolio Strategy Update:

As long-time members know, we don't spend a lot of time (almost none, actually) touting our views on the market or making "calls" about what to expect next. In our more than 40-years of combined market experience, we've learned that such efforts are at best a fool's errand and harmful to investors. You see, no one has been able to consistently "call" the market for any extended period. As such, we prefer to utilize a rules-guided approach.

With that said however, we are growing increasingly concerned about the mounting evidence regarding the potential for the current corrective phase to morph into a cyclical or "mini" bear market. While such declines have historically been shorter and shallower than your "average bear" (-23% vs. -32% on average over 8 months), we believe it is important to try and lose the least amount possible in our portfolios during bear market cycles.

So, despite the current rebound and the strong seasonal backdrop, we will be looking for opportunities to reduce exposure to risk. This was the primary reason we eliminated our position in QLD. By swapping the NASDAQ 100 index for the S&P 500, we reduced the beta of the overall portfolio. We expect to continue to take such action in the coming weeks.

The good news is that the BEST opportunities for gains in the stock market tend to occur as bear markets come to an end! So, while the coming months could prove challenging, keep in mind that a meaningful decline will likely lead to the next big bull opportunity.

The State of the Markets:

It's the first Friday of the month, which means it is time for the Big Kahuna of economic data - the jobs report. So, without further ado, let's get to the report and review the bevy of numbers.

The headline everyone focuses on new job creation for the month. The Bureau of Labor Statistics reported that Nonfarm Payrolls surged by 250,000 for October, which was well above the expectations for 190,000 - and is thus considered a big surprise to the upside.

As usual, there were revisions to the two previous reports. September's total, which was impacted by Hurricane Florence, was a bit of a surprise, being revised downward to 16K to 118K from 134K, while August's job gains saw an increase of 16K to 286K (from 270K). In sum, the adjustments were a wash.

The average monthly job gains over the past three months now stands at 218K (from 190K last month) and the average over the last two months is 184K. Both remain strong numbers.

Unemployment At Best Level Since Armstrong Walked on the Moon

The next big headline in the report was the nation’s unemployment rate, which came in at 3.7%. This was in line with the expectations for a reading of 3.7 and unchanged from last month's reading. Note that the current unemployment rate represents a 49-year low as the last time the rate was at 3.7% was December 1969.

The Inflation Implication

On the all-important inflation front, the government reported that wages grew by 0.2% in October, which was also in line with the Wall Street estimate and down from the 0.3% gain seen in September. And on the critical year-over-year view, wages are now up by 3.1% which was spot on the expectations and a 0.3% above last month's reading of 2.8%.

Note that the last time average hourly earnings grew at a rate above 3% on an annual basis was April 2009.

The "U6," which represents a broader measure of unemployment due to the fact that it includes "discouraged workers," fell to 7.4% from 7.5% in September (August: 7.4).

The Private Sector

Looking at the private sector (which does not include government jobs), the Labor Department says the economy created 246,000 new jobs last month. Recall that ADP reported Wednesday that, according to their tally, the private sector added 277,000 new jobs in October, which was well above the 230,000 new jobs last month (August: 163,000).

The Takeaway

This morning's report has to be considered "strong." However, the bears will argue that the data is actually too hot as it gives Jay Powell's Fed "cover" to continue with their plans for another rate hike in December and then three more in 2019. At issue here is the concern that growth is slowing and that an overly tight Fed will slow the economy unnecessarily.

Market Reaction

Market reaction has been conflicted. The yield on the 10-year jumped from 3.14% to 3.18% immediately following the report and is currently trading at 3.163%. Yesterday's closing yield was 3.136%.

The response in the stock market is a bit more complicated. Stock futures had been pointing to a gain of more than 300 Dow points prior to the report. The mood of the pre-market had been buoyed by word that China/U.S. trade relations might be thawing.

In addition to the tweet heard round the world where Trump talked about his "very good" phone conversation with Xi Jinping yesterday, this morning, Bloomberg is reporting that the President has asked for a draft of trade agreement terms. Thus, hope grows for a productive meeting between the heads of the U.S. and China at this month's G20 meeting.

However, around the time the Jobs report was released, questions were raised as to the validity of the Bloomberg report. And while it is difficult to tell which is the tail and which is the dog at this point in time, Dow futures now point to an open of about 200 points on the Dow.

In other news on this fine Friday morning, the world's largest company, Apple (AAPL), reported earnings that while at record levels and up more than 20% over year-ago levels, disappointed some analysts (quarterly guidance and the sustainability of growth appear to be the primary issues) and the stock is down 6% in pre-market trade. Thus, the iPhone maker is expected to be a drag on DJIA, NASDAQ, and S&P 500 indices today.

The bottom line is there is a lot for traders to digest here including earnings, rates, inflation, the state of the economy, jobs, the elections, and, of course, trade. And after a three-day bounce, investors shouldn't be surprised by any reaction in the stock market today.

Thought For The Day:

You can't build a reputation on what you're going to do. -Henry Ford

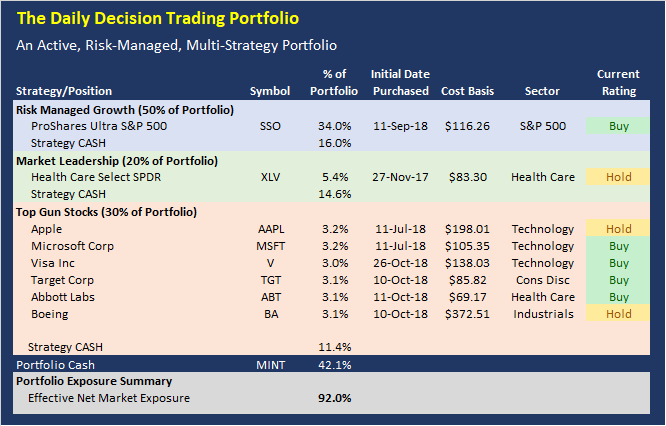

Today's Portfolio Review

Here is the current positioning of the portfolio and our member ratings:

Effective Net Market Exposure Explained

The Effective Net Market Exposure is the "net long" position of the overall model portfolio after factoring in the impact of leveraged long positions such as SSO and QLD and/or short positions. Leveraged ETFs such as SSO are designed to deliver approximately twice the daily return of the underlying index. Thus, a 10% holding in the SSO equates to a 20% "net long" position to the portfolio.

Current Rating Explained

This is our rating for the day. The Current Rating tells you what action we would take if we did not currently hold the position. A "Buy" rating means we would be willing to purchase the position at current prices. A "Strong Buy" suggests this would be our first choice to buy. A "Hold" rating indicates we would not make new purchases at current levels. And a "Sell" rating indicates we will likely exit the position in the near-term.

Positions Can Change

Positions often change during the trading session. Remember that we will send a Trade Alert via SMS Text Message and/or Email BEFORE we ever make a move in the models.

Disclosure

At the time of publication, the editors hold long positions in the following securities mentioned:

SSO, XLV, AAPL, MSFT, TGT, ABT, BA, WM, V

- Note that positions may change at any time.

About the Portfolio:

The latest upgrade to the Daily Decision service went live on Monday, July 9. The new, state-of-the-art portfolio employs a modern, hedge fund style approach incorporating multiple methodologies, multiple strategies, and multiple time-frames. The portfolio is comprised of three parts:

- 50% Aggressive Risk-Managed Growth (up to 300% long)

- 20% Market Leaders

- 30% Top Gun Stocks

The Aggressive Risk-Managed Growth portion is made up of five trading strategies and accounts for 50% of the portfolio. The Market Leadership portion makes up 20% of the portfolio. And the Top Guns Stocks portion (10 of our favorite stocks) will make up the final 30% of the portfolio.

All three of our strategies are run in a single Marketfy model - the model is currently labeled as the LEADERS model. The goal is to make the service simpler to follow by putting everything in one place.

Wishing You All The Best in Your Investing Endeavors!

The Front Range Trading Team

NOT INVESTMENT ADVICE. The analysis and information in this report and on our website is for informational purposes only. No part of the material presented in this report or on our websites is intended as an investment recommendation or investment advice. Neither the information nor any opinion expressed nor any Portfolio constitutes a solicitation to purchase or sell securities or any investment program. The opinions and forecasts expressed are those of the editors and may not actually come to pass. The opinions and viewpoints regarding the future of the markets should not be construed as recommendations of any specific security nor specific investment advice. Investors should always consult an investment professional before making any investment.

Recent free content from FrontRange Trading Co.

-

The Lines In The Sand Are Clear

— 9/16/20

The Lines In The Sand Are Clear

— 9/16/20

-

The Question of the Day

— 8/04/20

-

Portfolio Update: 1.23.20

— 1/23/20

-

State of the Markets: Modeling 2020 Expectations (Just For Fun)

— 1/13/20

-

Current Holdings for ALL-NEW 2020 Daily Decision Model Portfolio

— 1/03/20