The NEW Daily Decision for 10.8.18 - Time To Hit Reset?

The State of the Markets:

As long-time readers are aware, the main objective of my oftentimes meandering market missive is to identify the driving forces behind the action in the stock market. For the past 20+ years, my thinking has been that if I can stay in tune with what is happening and why in Ms. Market's game, I may be able to avoid getting fooled badly when something really big happens.

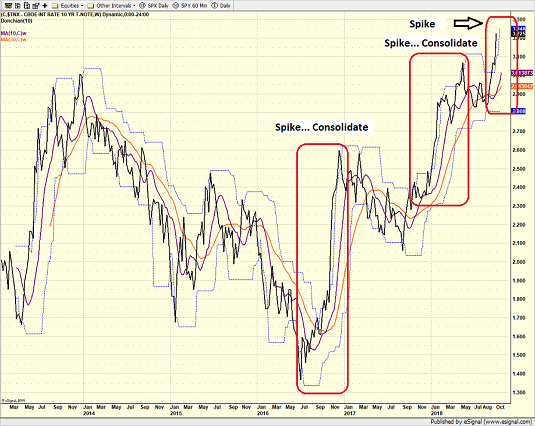

In looking back at the week that was, it is clear (as in "crystal") that the most recent spike in interest rates was the driving factor in the stock market action. In just five trading sessions, the yield on the U.S. 10-year went from 3.056% to 3.225%, which represents (a) a new high for the year, (b) a breakout to a new cycle high, and (c) the highest level seen since April 2011. So, yea, it was a pretty big deal.

As the chart below illustrates, this is simply the latest in a string of spikes that began in mid-2016.

S&P 500 - Daily

View Larger Image Online

It is also worth noting that the spikes tend to be swift and are then followed by a period of consolidation.

So, the logical questions become: Why did rates spike? And why now?

Cutting to the chase, I believe that a reset in expectations from a macro perspective and some pretty important comments from some pretty influential folks were the primary reasons behind the big move in the bond market. You see, suddenly everyone is worried that the Fed will be forced to overshoot and that when combined with a prolonged trade war, higher rates could become a drag on economic growth.

From my seat, the keys to the surge in bond yields included a round of stronger economic data, technical breaks, and comments from the likes of Powell, Warsh, Gundlach, and Hatzius. So, let's run it down.

Better Than Expected

First up is the economic data. The bottom line here simple. While everybody knows the economy is doing just fine, thank you, last week's ISM Non-Manufacturing, ADP, and Nonfarm Payroll reports all raised eyebrows.

For example, the ISM services index came in at 61, which was leaps and bounds better than the expected level of 58. Analysts were also fooled by the ADP report as private sector payrolls were significantly higher than consensus. And then the monthly jobs report sported the lowest level of unemployment since December 1969. Yowza.

At first blush, all of the above certainly sounds good. But unfortunately, we are at that stage in the game where the data was perhaps a bit too good.

He Said, What?

While likely not directly in response to last week's data, comments from Fed Chairman Jerome Powell and former Fed Governor Kevin Warsh also appeared to get bond traders fired up.

First, Powell told PBS that "really extremely accommodative low interest rates" are "not appropriate" anymore. Frankly, this shouldn't have surprised anyone. However, the next comments the Fed Chair made certainly did.

First, Powell said that rates may go higher than the markets currently expect. Specifically, the Fed Chairman said, "We may go past neutral." The issue here is markets have been expecting the Fed to stop raising rates once the "neutral" level in the Fed Funds Rate is achieved. This was the first traders have heard about the potential for rate hikes to continue past the neutral zone.

Then, on the subject of what "neutral" actually means, Powell added, "we're a long way from neutral at this point." Again, the key is this appeared to take traders by surprise.

Yes, there is a chance that this was taken out of context as the current consensus for "neutral" is 3% on the Fed Funds Rate. And since it can be argued that 3% is indeed a long way from the current range of 2.0% - 2.25%, perhaps traders overreacted.

Next up were the comments on inflation from Kevin Warsh. The former Fed Governor said the labor market is "booming" and that wage pressures are visible everywhere except in the government data. As such, Warsh opined that wage pressures will begin showing up in the near future. And lest we forget, wages are the toughest part of inflation for the Fed to fight.

Oh, and in case you missed it; Ned Davis Research declared that the bear market in bonds has finally arrived. (But for the record, NDR is waiting for German yields to confirm in order to officially declare the bond bear intact.)

Speaking of big calls, the new "Bond King" - aka Jeffrey Gundlach - pointed out on Friday that he was indeed right back in the summer of 2016 when he declared the low point in bond yields had been seen and that a bear was upon us. Mr. Gundlach also suggested that "significantly higher bond yields" are ahead.

Finally, Goldman's Chief Economist, Jan Hatzius summed up the situation nicely Friday when he told CNBC that the Fed is likely to continue to hike rates and probably by more than the markets are currently pricing in.

Time To Hit Reset?

So there you have it; a nearly perfect storm for the bond bears. And with key technical levels snapping like toothpicks, bond buyers were simply overrun by sellers last week.

And as a result of the data and the commentary, traders may now be in the process of rethinking their base case macro scenario going forward. And the bottom line is this "reset" in expectations may include higher rates and higher inflation. Neither of which has not been particularly kind to stocks in the past.

Moving On... Now let's turn to the weekly review of my favorite indicators and market models...

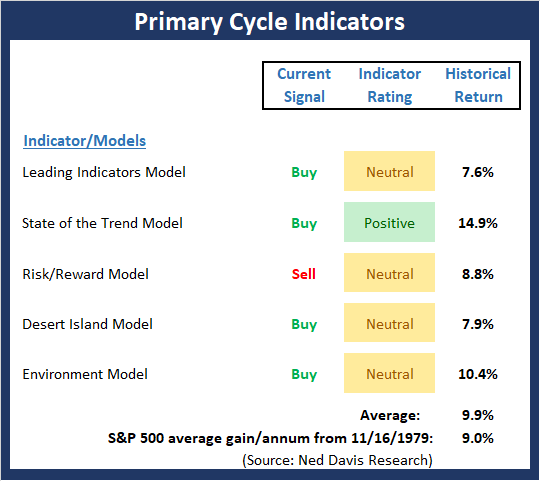

The State of the Big-Picture Market Models

I like to start each week with a review of the state of my favorite big-picture market models, which are designed to help me determine which team is in control of the primary cycle.

View My Favorite Market Models Online

The Bottom Line:

-

A quick glance at the Signal column and the colors of the indicator rating boxes says it all about Primary Cycle board this week. While there were no signal changes, the readings of the State of the Trend and Desert Island model both slipped into the neutral zone with the State of the Trend reading at its 2nd lowest level of the year.

This week's mean percentage score of my 5 favorite models slipped a bit to 55.5% while the median held steady at 65%. The current readings suggest to me that the underlying strength of the overall market structure continues to falter.

The State of the Trend

Once I've reviewed the big picture, I then turn to the "state of the trend." These indicators are designed to give us a feel for the overall health of the current short- and intermediate-term trend models.

View Trend Indicator Board Online

The Bottom Line:

- The status of the Trend Board slipped a bit this week as the short-term trend indicators broke down. FYI, the Cycle Composite points slightly lower this week and then up for the next two. The question of the day is if the "generals" (Dow/S&P 500) will follow the "troops" (small-, mid-caps) into full-fledged downtrends. The divergence here continues to warrant some attention.

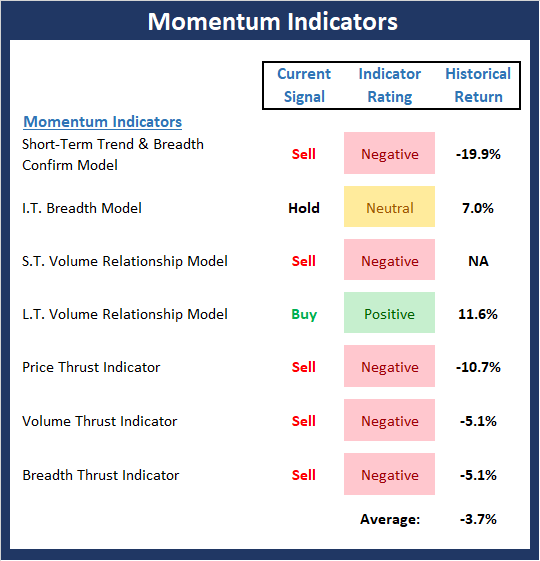

The State of Internal Momentum

Next up are the momentum indicators, which are designed to tell us whether there is any "oomph" behind the current trend.

View Momentum Indicator Board Online

The Bottom Line:

- With only a single "buy" signal currently on the board, Momentum has to be considered a problem. Three indicators on the board fell into the red this week (I.T. Breadth, S.T. Volume Relationship, and Breadth Thrust Indicator) and only the longer-term volume relationship indicator remains on a buy signal.

The State of the "Trade"

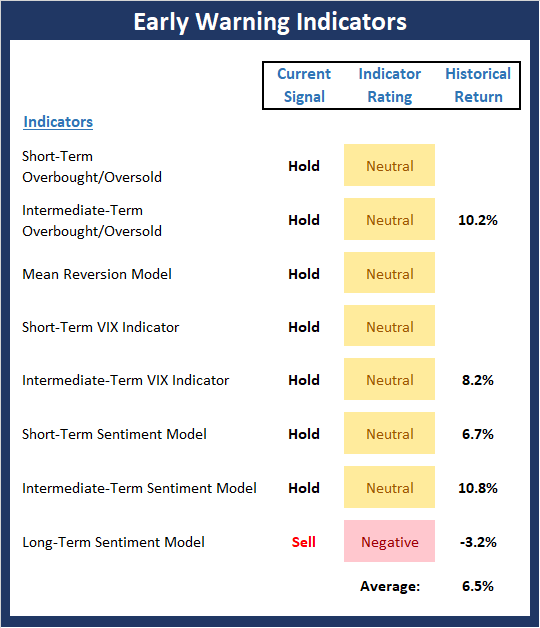

We also focus each week on the "early warning" board, which is designed to indicate when traders might start to "go the other way" -- for a trade.

View Early Warning Indicator Board Online

The Bottom Line:

- The "Early Warning" board did a nice job of signaling that the bears were due to get in the game recently. However, the overbought/overbelieved tailwinds have now waned and the board is clearly neutral.

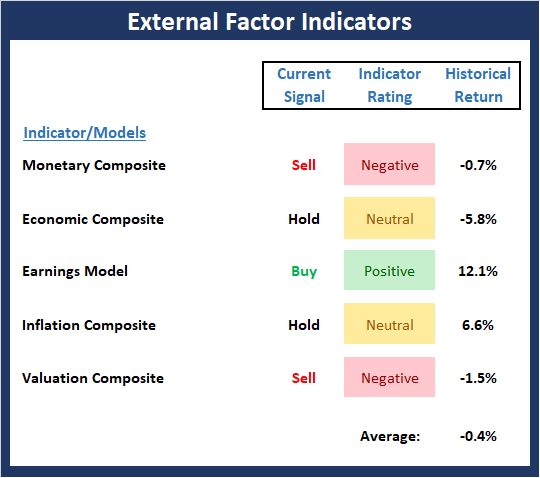

The State of the Macro Picture

Now let's move on to the market's "environmental factors" - the indicators designed to tell us the state of the big-picture market drivers including monetary conditions, the economy, inflation, and valuations.

View Environment Indicator Board Online

The Bottom Line:

- The External Factors board continues to suggest that this is not a low risk environment and that some degree of caution is warranted.

Thought For The Day:

Commitment means staying loyal to what you said you were going to do, long after the mood you said it in has left you. -Inky Johnson

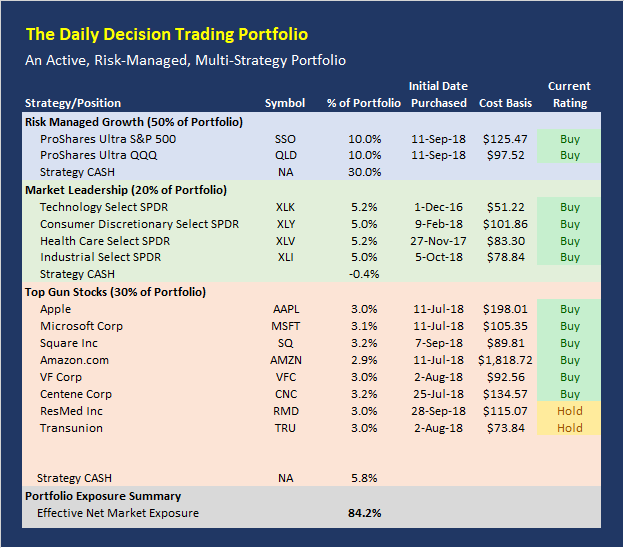

Today's Portfolio Review

Quick Take: The portfolio is currently in a modestly defensive stance with 84% net long exposure (out of a possible 200%). The key question at this point is if we are seeing the beginning of a new corrective phase or just another dip. Stay tuned.

2018 YTD Performance Update:

Daily Decision Portfolio: +8.1%

S&P 500: +7.9%

Current Rating Explained

This is our rating for the day. The Current Rating tells you what action we would take if we did not currently hold the position. A "Buy" rating means we would be willing to purchase the position at current prices. A "Strong Buy" suggests this would be our first choice to buy. A "Hold" rating indicates we would not make new purchases at current levels. And a "Sell" rating indicates we will likely exit the position in the near-term.

Positions Can Change

Positions often change during the trading session. Remember that we will send a Trade Alert via SMS Text Message and/or Email BEFORE we ever make a move in the models.

Disclosure

At the time of publication, the editors hold long positions in the following securities mentioned:

SSO, QLD, XLK, XLY, XLV, AAPL, MSFT, AMZN, CNC, TRU, VFC, SQ, RMD

- Note that positions may change at any time.

About the Portfolio:

The latest upgrade to the Daily Decision service went live on Monday, July 9. The new, state-of-the-art portfolio employs a modern, hedge fund style approach incorporating multiple methodologies, multiple strategies, and multiple time-frames. The portfolio is comprised of three parts:

- 50% Aggressive Risk-Managed Growth (up to 300% long)

- 20% Market Leaders

- 30% Top Gun Stocks

The Aggressive Risk-Managed Growth portion is made up of five trading strategies and accounts for 50% of the portfolio. The Market Leadership portion makes up 20% of the portfolio. And the Top Guns Stocks portion (10 of our favorite stocks) will make up the final 30% of the portfolio.

All three of our strategies are run in a single Marketfy model - the model is currently labeled as the LEADERS model. The goal is to make the service simpler to follow by putting everything in one place.

Wishing You All The Best in Your Investing Endeavors!

The Front Range Trading Team

NOT INVESTMENT ADVICE. The analysis and information in this report and on our website is for informational purposes only. No part of the material presented in this report or on our websites is intended as an investment recommendation or investment advice. Neither the information nor any opinion expressed nor any Portfolio constitutes a solicitation to purchase or sell securities or any investment program. The opinions and forecasts expressed are those of the editors and may not actually come to pass. The opinions and viewpoints regarding the future of the markets should not be construed as recommendations of any specific security nor specific investment advice. Investors should always consult an investment professional before making any investment.

Recent free content from FrontRange Trading Co.

-

The Lines In The Sand Are Clear

— 9/16/20

The Lines In The Sand Are Clear

— 9/16/20

-

The Question of the Day

— 8/04/20

-

Portfolio Update: 1.23.20

— 1/23/20

-

State of the Markets: Modeling 2020 Expectations (Just For Fun)

— 1/13/20

-

Current Holdings for ALL-NEW 2020 Daily Decision Model Portfolio

— 1/03/20

{kind=link}